Recent Search

Popular Searches

As the US economy benefits from the USD 1.9trn American Rescue Plan and a strong pace of Covid-19 vaccinations, its growth differential to major peer economies is improving. We expect that strength to play out now more considerably in FX markets with EURUSD and USDJPY set to experience sustained periods of dollar strength. Among the other majors we are more optimistic for their chances against the greenback given the sounder fundamentals at play and, for the commodity currencies in particular, their gearing toward improving global growth trends.

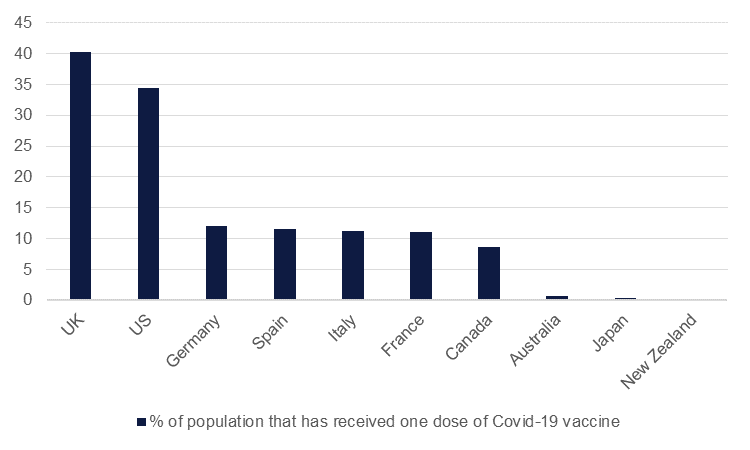

Vaccination programmes across major EU members are proceeding at a halting pace, particularly when compared with the UK or US. Germany has had the most success among the large EU economies but has so far provided less than 12% of its population with a dose of a Covid-19 vaccine compared with nearly 40% in the UK and almost 35% in the US. France, Spain and Italy are all lingering at around 12% of their population having received a dose.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

The EU is also now putting up more barriers to achieving its vaccination goals as many members have halted the use of the AstraZeneca vaccine. Meanwhile, case numbers across some major economies have been increasing rapidly in recent weeks: both Germany and Italy have experienced a notable upward pull in their seven-day average new case numbers while the stringency of Covid-19 restrictions in Italy, France, Germany, Spain and the Netherlands are nearly as high as they were in Q2 2020.

The European Commission has said it will outline a tiering system for when countries can begin to remove lockdown measures but considering that the EU is now putting up more blocks on vaccinations rather than easing access to them, we are doubtful that restrictions could be removed in a meaningful way in H1 2021.

The so far tentative rollout of vaccines in the EU is weighing on a growth outlook already beset by difficulty. The Eurozone’s economy contracted by 6.6% in 2020, considerably more than the US, and is likely to endure another contraction in Q1 2021. Despite managing to agree a EUR 750bn recovery plan during the middle of 2020, national spending plans have yet to be approved by the Commission, delaying getting the much-needed funds into the economy. That’s left the ECB as the Eurozone’s primary economic agent and there the commitment remains keeping policy accommodative, if not necessarily at this stage to expand the overall EUR 1.85trn target of the Pandemic Emergency Purchase Programme.

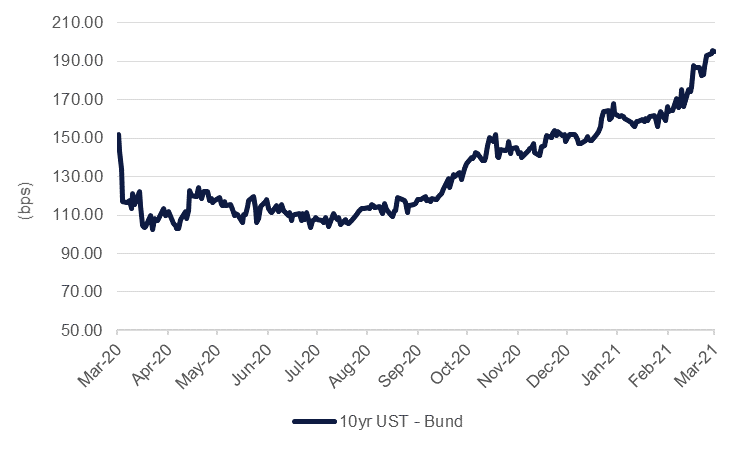

Growth differentials are widening considerably in favour of the US relative to the Eurozone along with a sizeable deterioration in 10yr nominal bond spreads that favour USTs over bunds. We do believe that the bearishness in UST markets is a little overwrought at present but a wide yield differential in favour of USTs vs Eurozone bonds remains sound given the economic divergence between the two.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

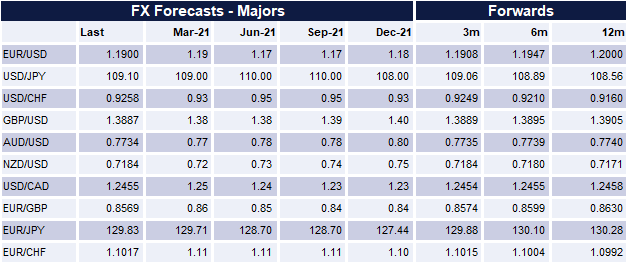

We expect to see further downside for the EURUSD pair in the current market conditions, targeting it reaching 1.17 in Q2 – Q3 before a modest gain by the end of the year as vaccination programmes should have reached critical mass and allow for improvement in the Eurozone economy.

For USDJPY, we don’t expect the Bank of Japan to step in the way of a weaker yen as it will flatter exporters and may help to firm up inflation expectations for the economy. Japan is at an early stage in its vaccination programme with just 0.2% of the population having received at least one dose of a Covid-19 shot and its economy will underperform the US by even a wider margin than the Eurozone.

Japan’s government extended massive stimulus to support the economy in 2020 and the appetite for more widescale spending seems limited this year. Stimulus this year has so far been limited to low-income households receiving cash handouts while a strategy review from the BoJ is unlikely to push the bank away from yield curve control aiming to keep long-term rates low.

We see more upside from here for USDJPY with a test of 110 possible over Q2- Q3. Should financial markets acquiesce to the reflation trade, that should also help to keep pressure on the yen as investors dump low yielders.

GBPUSD has had a resounding start to the year, benefitting from early mover advantage in vaccination even as lockdown measures remain in place until June. Bank of England governor Andrew Bailey also seems to be viewing the rise in gilt yields as an endorsement of the UK’s growth outlook rather than a premature tightening of financial conditions.

The wide level of vaccination and accumulated savings should mean that when lockdown measures are lifted in the summer a pop in activity should be noticeable. GBPUSD has pulled back from exuberant levels of more than 1.42 set earlier this year but that sets the pair up to be supported on a more sustained basis over the rest of the year even as the UK economy is still likely to have contracted in Q1.

Source: Bloomberg, Emirates NBD Research.

Edward Bell

Edward Bell