Recent Search

Popular Searches

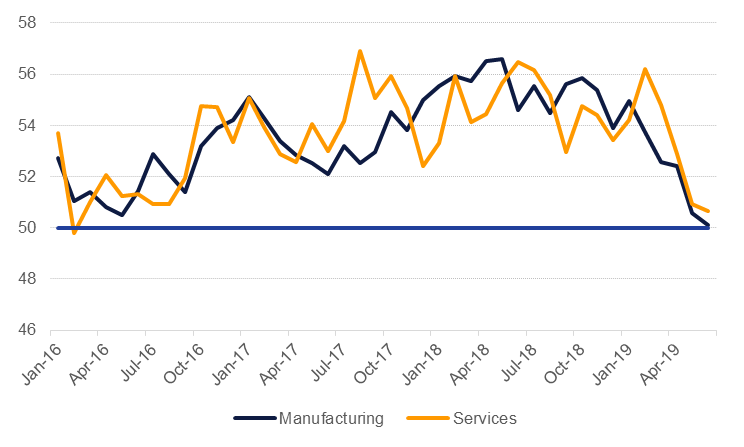

The US manufacturing PMI weakened to just 50.1 in its June print, barely holding above the neutral 50 level. The PMI figure was a slowdown from 50.5 only a month earlier and much healthier levels of around 55 for much of the last 18 months. The deterioration in trade relations between the US and China will be weighing on business attitudes toward growth and will start to feed in higher input costs as US firms pay the cost of higher tariffs, not China as the US president appears to believe. All eyes on the upcoming G20 meeting at the end of the week will be fixated on dialogue between Donald Trump and Xi Jinping, his Chinese counterpart, as to whether trade talks will resume. While an all-encompassing trade deal is not likely to emerge this week, some kind of positive engagement will provide relief to markets. We would caution though that for President Trump, maintaining a hawkish stance on China trade issues will be a popular political agenda during his 2020 reelection bid.

PMI data for the Eurozone showed some positive news as the headline composite index recorded a flash print of 52.1, up from 51.8 in May. There is still mixed performance country by country in the Eurozone as German manufacturing continues to linger below 50, weighing on overall conditions. The upswing in data follows on from dovish commentary from ECB chief Mario Draghi who said the bank would add stimulus unless data improved. Should economies have to endure further months of trade uncertainty the chances of more ECB stimulus, in our view, become much stronger later in the year.

The Bank of England voted unanimously to keep rates on hold at its MPC meeting last week. However, like in other central banks, bias at the BoE is tilting toward keeping rates on hold for longer rather than further hikes. Uncertainty linked to Brexit, a leadership contest underway in the Conservative party and broader global trends will all weigh on the outlook for the relatively outperforming UK economy.

Source: Haver, Emirates NBD Research

Source: Haver, Emirates NBD Research

Treasuries closed higher as the Federal Reserve game ample indications that the central bank remains ready to cut interest rates. This coupled with escalation in geopolitical tensions drove safe haven buying in USTs. The curve steepened and yields on the 2y UST, 5y UST and 10y UST ended the week at 1.76% (-8 bps w-o-w), 1.79% (-4 bps w-o-w) and 2.05% (-3 bps w-o-w).

Regional bonds closed higher following the move in benchmark yields. The YTW on Bloomberg Barclays GCC Credit and High Yield index dropped -10 bps w-o-w to 3.63% and credit spreads tightened 6 bps w-o-w 168 bps.

In terms of rating action, S&P affirmed the rating of ABNIC at BB+ with outlook still remaining negative.

The dollar’s decline over the last week is technically significant. The declines have taken the index below the formerly supportive 100-day moving average (97.115), 200-day moving average (96.631), and 61.8% one-year Fibonacci retracement (96.592). With these areas likely to now provide resistance, risk is that while the price remains lower than the 96.50 level, the index may see a further decline towards the 95.50 level. This probability of this occurring will be magnified if there is a daily close below the 50% one-year retracement of 96.042.

Regional markets started the week on a negative note as investors turned cautious in light of escalating geopolitical tensions. The DFM index and the Qatar Exchange lost -0.7% and -1.3% respectively. The sell-off was broad based with all market heavyweights closing in negative territory.

Oil markets remain transfixed by the escalation in tension between the US and Iran and the impact heightened geopolitical risks could have on flows of crude oil out of the Gulf region. Brent futures rose more than 5% over the week to close at USD 65.20/b, with much of the gain occurring thanks to a more than 4% jump on Thursday in response to news that a US military drone was shot down. WTI futures rose almost 10%, abetted by a draw in US crude inventories.

OPEC has finally agreed to meet at the start of July after weeks of dithering on when or if to hold a meeting. There appears to be broad consensus within OPEC on the need to extend the current round of production cuts into H2 but doubt on whether Russia will continue to support the cuts. Our expectation is for OPEC producers to roll over the cuts but that output will increase to closer to targeted levels as there is ample room to increase. Saudi Arabia production in May was 260k b/d lower than its target, according to Reuters estimates. But producers in OPEC will be reticent to appear to respond to any US call to increase production and keep prices stable after their experience in 2018 when the effect of output increases was undercut by the US providing Iranian crude export waivers.

Edward Bell

Edward Bell