Recent Search

Popular Searches

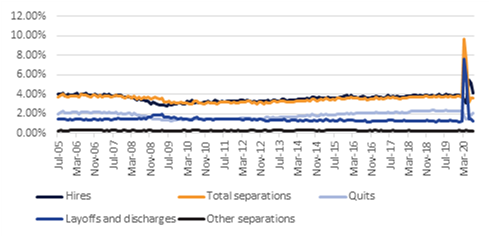

The U.S. Labor Department released the Job Openings and Labor Turnover Survey (JOLTS), which showed job openings rising 617,000 to 6.6 million in July. Vacancies increased within trade, transportation and utilities sectors, as well as in construction, education, healthcare and business services. Vacancies in the leisure and hospitality sector declined on the back of still weak demand due to the pandemic. The quits rate increased to 2.1%, the highest since February as more workers quit their jobs in the retail as well as professional and business services industries due to exposure to COVID-19 and challenges with childcare.

The Bank of Canada held its key overnight interest rate steady at 0.25%, saying recovery in the third quarter was likely to be faster than previously anticipated. However, the central bank noted that as the Canadian economy moves from the recovery phase to a recuperation phase it will continue to require extraordinary monetary policy support. Canada will this month start to transition people off its main COVID-19 emergency income support program and onto traditional unemployment benefits, which will likely bring headwinds to already nascent consumer spending. The central bank also noted that both the global and Canadian economies are progressing broadly in line with the scenario it set out in July, adding that the rebound in the US, which is Canada's largest trading partner, is stronger than expected.

The UAE’s CPI declined -0.6% m/m (-2.1% y/y) in July, slower than the -2.4% y/y deflation recorded in June. Both food and housing costs declined m/m; these two components account for almost half of the CPI basket. There was a notable drop of -14.5% m/m (-31.6% y/y) in “recreation & culture” prices which likely reflects discounts to leisure attractions and entertainment services as these services reopened following the further easing of coronavirus restrictions in July.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

US treasuries were largely unchanged yesterday, with the two-year flat at 0.1468% while the 10-year added two basis points to 0.7001%. In the UK, the two-year gilt rose modestly from the all-time low it hit on Tuesday to -0.83%.

Expectations that the ECB will talk up easing monetary policy at today’s meeting have dampened after officials have become more confident, and only modest adjustments to their economic forecasts are expected. Even were the ECB to act, an extension to its QE would be the more likely scenario for now, rather than a rate cut further into negative territory.

The USD's recent rebound faltered on Wednesday. The DXY index looked to consolidate gains established in the previous two sessions, but fell by -0.30% in the evening and currently trades at 93.160. Despite broad-based USD weakness, the JPY experienced a minor increase to reach 106.10.

The USD's shortcomings have provided a boost for most major currencies paired against it. The euro earned modest gains and is hovering 1.1824. GBP earned some respite from recent weakness, remaining largely unchanged around the 1.30 handle. Meanwhile the AUD and NZD advanced by 0.78% and 0.97% to trade at 0.7270 and 0.6685 respectively.

Equity indices rebounded yesterday, despite negative news regarding the development of the AstraZeneca vaccine in the morning. All three major US indices were up, with the S&P 500, the Dow Jones and the NASDAQ gaining 2.0%, 1.6% and 2.7% respectively – although they remain down w/w. In Europe, the FTSE 100 closed at its highest level in two weeks, gaining 1.4%, while the CAC and the DAX climbed 1.4% and 2.1%.

The day was more bearish in China, where contagion from the US tech slump, fears over rising US-China tensions, and questions regarding a potential rollback of liquidity boosts after positive economic data saw the Shanghai Composite lose 1.9%. However, the index is trading higher this morning.

The return of risk-on sentiment which bolstered equities yesterday also saw oil markets bounce following their previous declines, with WTI futures closing 3.5% higher at USD 38.05/b, while Brent gained 2.9% to end the session at USD 40.79/USD. However, both benchmarks are trending lower once more in early morning trading today, following news that US inventories surged again following six consecutive weeks of declines. According to the API, US crude stocks rose by 2.97mn barrels last week, which alongside the end of the traditional US driving season, and ongoing questions regarding the strength of the economic recovery, will increase pressure on oil prices.