Recent Search

Popular Searches

President Donald Trump withdrew the US from the JCPOA, the Iran nuclear deal, and ordered the Treasury and State Departments to re-impose sanctions on Iran that were lifted in 2016. The first round of sanctions will come into effect in 90 days targeting purchases of US dollars by the Iranian government and specific trade in metals and Iran’s car industry. After 180 days, the US will begin to impose sanctions related to Iran’s sale of crude oil and the Treasury Department has specifically noted it will take steps to actively reduce Iran’s crude exports.

We had anticipated that the US would withdraw from the JCPOA and president Trump has taken a more aggressive approach to dealing with Iran than many in the market had likely expected. The European signatories to the deal have announced they would still abide by the terms and not impose their own sanctions: EU sanctions on insurance were particularly effective in disrupting Iranian exports when they were imposed in 2012. However, even if the EU does not follow the US’s lead in re-imposing sanctions, EU-based companies may seek to cut back on purchases of Iranian crude to avoid penalties.

Source: Eikon, Emirates NBD Research

Source: Eikon, Emirates NBD Research

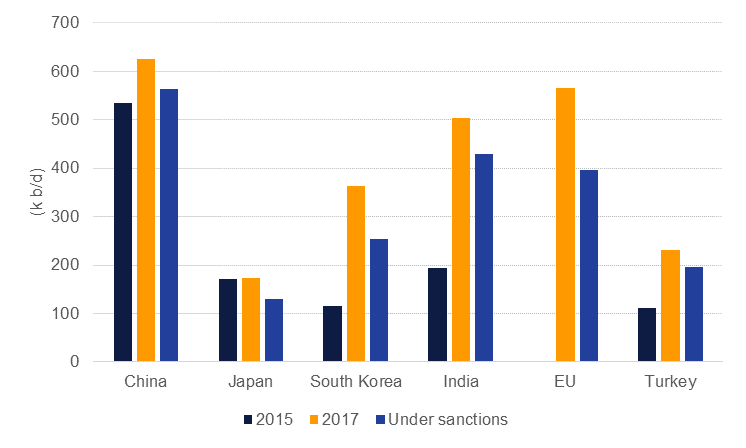

In the immediate aftermath of the US withdrawal the impact on oil markets will be relatively limited and we expect a marginal cut in exports in Q2. Indeed, Iranian crude exports have been running at elevated levels in recent months so some modest pull back may be on the cards. However, from the second half of the year onward we expect the oil market will feel the full impact of the Iran sanctions more significantly. According to the Treasury Department, if companies want to remain exempt from sanctions they will need to demonstrate ‘significant reductions’ during the 180 wind-down period and not seek to enter into new contracts to import Iranian crude.

Of the more than 1m b/d increase in exports Iran was able to achieve after sanctions were lifted, we expect at least 500k b/d will be cut by the end of the year. Iran’s oil production will fall by over 4% this year but the full impact of lower volumes will be felt in 2019 as importers continue to cut their imports.

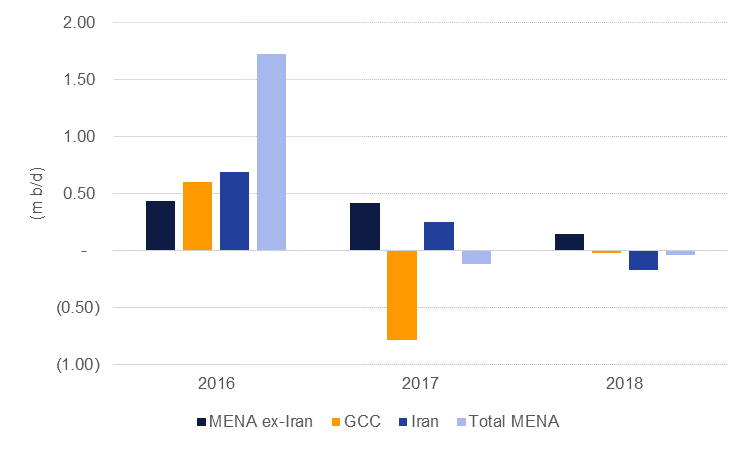

We expect that other members of OPEC will adjust production to compensate for the disruption to Iranian volumes but it won’t be sufficient to offset all of the decline in Iran’s output. Saudi Arabia is likely to adjust output only in coordination with other producers in OPEC and we expect that it will only raise output so that it is 100% compliant with the terms of the OPEC production cut agreement (Saudi Arabia has been over-cutting and thus hitting its target would mean higher output). For the UAE, hitting 100% compliance means production can increase from the low levels recorded in Q1 but in year on year terms output will still be lower (2.2%) considering its failure to hit targeted levels in 2017. Production from the GCC had been lower than we anticipated to start the year as producing nations sought to aggressively draw down inventories and target higher prices. On an aggregate MENA basis, overall production growth from the region will be close to flat in 2018 even with increasing output in H2.

Source: IEA, Emirates NBD Research. Note: oil production growth (m b/d).

Source: IEA, Emirates NBD Research. Note: oil production growth (m b/d).

OPEC’s next meeting is scheduled for June and how the producers’ bloc will address the unanticipated outages from Venezuela and Iran will likely be a critical part of the agenda. Were OPEC to announce that they are dismantling the deal early oil prices would most likely slump, even taking into account the lower volumes from Iran and Venezuela, and hence we doubt OPEC would be prepared to endorse an early exit from the deal.

Our lower forecast for Iranian oil production with limited offsetting output from OPEC has reshaped our projections for overall oil market balances and we now expect a much deeper deficit in H2 2018 of around 600k b/d. A deficit this wide will help to push days of forward cover in OECD stocks back below the +60 days they have recorded in 2015-17 and closer to their long-term average of around 55 days.

Source: IEA, Emirates NBD Research

Source: IEA, Emirates NBD Research

Consequently we are revising our oil market forecasts and now anticipate that Brent crude futures will record an average of USD 69/b in 2018. A potential move to as high as USD 80/b appears possible in the current climate. Prices should begin to taper off slightly by the end of the year even with a relatively wide market deficit as we think the risk of a broader slowdown in global growth will become more apparent by the end of 2018, weighing on commodity prices. We expect that WTI prices will also move higher in line with Brent and record an average of USD 65/b this year.

Our 2018 GDP growth forecasts had assumed a much lower level of compliance with OPEC production targets than has been evident so far this year. Consequently, the downward revisions to annual oil production estimates will result in slower GDP growth for the main GCC exporters.

In Saudi Arabia’s case, we are now looking for just 0.5% increase in oil production in 2018, compared with a forecast of 1.5% for oil sector growth at the start of this year. Non-oil sector growth – as reflected in the PMI surveys - has also been weaker than we had anticipated year-to-date, and we have revised down our 2018 growth forecast for the Kingdom to 1.5% from 2.5% previously.

For the UAE, we had assumed a 2.0% rise in crude oil production in 2018 at the start of this year, which contributed to an overall real GDP growth forecast of 3.4%. However, given the sharp decline in UAE oil production year-to-date, even a modest increase in output to the OPEC agreed target for the rest of 2018 implies that on average, the UAE’s oil sector will contract by more than -2.0% in 2018, shaving more than a full percentage point off our real GDP growth forecast.

On the positive side, higher oil prices will significantly boost oil revenues, helping to narrow budget deficits and widen current account surpluses in the GCC in 2018.

If we pencil in a reduction in Iranian oil production of 500k b/d on the back of the renewed sanctions (compared to nearly 1m b/d last time), a 2% real contraction in Iran’s GDP is feasible in 2019. The impact of the lower oil exports would not be as severe as that seen in 2012, given that the volume being lost is halved, and the oil sector in any case represents a smaller proportion of GDP than it did previously. In 2011 the oil sector accounted for around a quarter of GDP, but in 2017 the oil sector accounted for just 13% of GDP even as production recovered, demonstrating how the years of sanctions have forced the Iranian economy to diversify.

It is not only the oil sector which will be hit by renewed sanctions, but other exports will also be limited. Although the European signatories of the deal might look to maintain their relations with Iran, trade will certainly be constrained by the US sanctions. Private sector firms such as Renault, Total, Boeing and Airbus will likely see their activities in Iran nullified, and increasing numbers of foreign firms will look to withdraw their capital from the country. That being said, the threat of renewed sanctions against Iran has loomed since President Trump’s election victory in 2016, and the inflow of foreign investment has already been far slower than the Iranian authorities hoped – another reason why the impact of these renewed sanctions would not be as great as seen in 2012, when the economy contracted by 7.8%.

It will not only be international firms that will seek to withdraw their money from Iran. According to MP Mohammad Pourebrahimi, USD 30bn was transferred out of the country by Iranians in the last several months of the Iranian year ended March 20, and many are storing dollars at home. This will likely be exacerbated by the latest developments, leading to a renewed sell-off of the rial, even despite government efforts to make this illegal. In April, a sharp depreciation to IRR 60,000/USD on the parallel market led the authorities to impose a new rate of IRR 42,000/USD and threats to prosecute anyone caught selling the currency for anything less. The renewal of sanctions will likely eventually force the authorities to make further sizeable devaluations to the official rate, to at least IRR 60,000/USD in our view. This would in turn see inflation accelerate once more.

Click here to Download Full article

Edward Bell

Edward Bell