Recent Search

Popular Searches

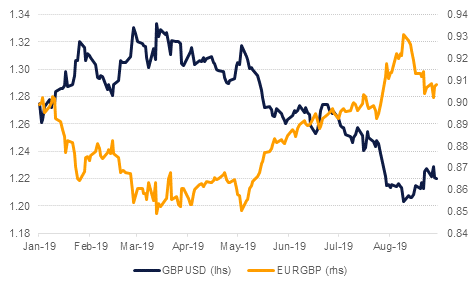

Brexit has entered a new phase as UK prime minister Boris Johnson will suspend parliament for several weeks just ahead of the October 31st Brexit deadline. Parliament is set to return from recess next week and will only have a few short sessions before it is suspended to allow time for a Queen’s Speech, an official opening of parliament. Parliament would only then resume its sessions in mid-October. MPs would only then have a few days to debate any new deal or changes to the existing withdrawal agreement before the UK leaves the EU. Opposition parties in the UK are trying to coalesece around some form of anti-hard Brexit coalition and there is chance they could use a vote of no confidence, as early as next week, to force an election. Were parties to enter into an election cycle we doubt that any pending cooperation between the Labour and Liberal Democrat parties would endure and the next parliament would have no party anywhere near a majority. As Brexit enters its final days with even more uncertainty, UK assets tumbled; sterling moved back below 1.22 against the USD although it did later recoup some ground while gilt yields edged lower throughout the day.

Consumer inflation in Saudi Arabia rose just 0.1% m/m in July, as higher transport, healthcare and household furnishing prices were offset by lower food and clothing costs. On an annual basis, the cost of living index remained in deflation territory at -1.4% y/y. Lower housing costs have been the main driver of deflation over the last year, accounting for more than 20% of the consumer basket. We expect inflation to average -1.0% this year, before recovering to 2% in 2020.

Turkish economic confidence rose to 87.1 in in September, a 12-month high and up 7.9% from 80.7 in July. The improvement was broad-based across all sectors measured by the survey, with services leading the gains with a m/m increase of 6.7% to 89.1. Nevertheless, the index remains far off the 10-year average of 100.0 as the economy continues to grapple with the fallout of last year’s lira sell-off.

Italy moved a step closer to resolving its political crisis with the 5-Star Movement and Democractic Party agreeing to form a coalition. The incumbent prime minister, Giuseppe Conte, has been summoned by Italy’s president for a meeting today in the likelihood he will be asked to form a government. Yields on 10yr Italian bonds moved below 1% yesterday, a record low, while spreads over equivalent Bunds narrowed to just 174bps.

Source: Emirates NBD Research

Source: Emirates NBD Research

Treasuries closed higher following sharp gains in European bonds. However, they continued to trade within this week’s range. The curve steepened and yields on the 2y UST, 5y UST and 10y UST closed at 1.50% (-2bps), 1.37% (flat), 1.47% (flat).

In Europe, yields on the 10y Italian bonds dropped 9bps to 0.98% as a new coalition was formed. In the UK 10y Gilts fell 6 bps after Prime Minister Boris Johnson moved to suspend Parliament, boosting odds of a no-deal Brexit.

Regional equities continued their positive run. The YTW on Bloomberg Barclays GCC Credit and High Yield index dropped -4 bps to 3.08% and credit spreads continued to remain in a tight range around 161 bps.

Sterling slumped on news that the UK parliament will be suspended just weeks ahead of the October 31st Brexit deadline. GBP closed down 0.6% at 1.2209 although it did push below the 1.22 handle briefly. Elsewhere, trade exposed currencies remain exposed to the uncertainty over whether US-China trade talks will resume with both the AUD and NZD losing ground.

The CNY moderated its losses overnight but did extend its losing streak to 10 days in a row and is edging softer this morning. The PBOC continues to try and support the redback by setting the official mid-rate at stronger than market expectations.

US Treasury Secretary Steve Mnuchin said the US would not intervene in FX markets at this stage as there is seemingly little support from the Fed for such a move. US President Donald Trump has loudly complained about the strength of the dollar and called on the Fed to cut rates.

Developed market equities closed mixed as worries over global growth remain. However, a sharp rally in oil prices helped investor sentiment. The S&P 500 index and the Euro Stoxx 600 index closed +0.7% and -0.2% respectively.

Regional equities closed mixed. The Tadawul dropped -1.4% as the impact of second phase of inclusion in the MSCI EM index plays out. Elsewhere, the DFM index gained +0.2% on the back of strength in Emaar Properties which closed +1.0% higher. Egyptian equities too saw a sharp rally with the EGX 30 index gaining +2.2%.

Oil markets remained bid overnight as the EIA reported a large draw in crude stocks, helping to take Brent back above USD 60/b and WTI within sight of USD 56/b. Total crude stocks in the US fell by 10m bbl last week, nearly in line with the API’s earlier estimate, as imports fell by 1.3m b/d. Total product and crude stocks reported their first overall draw in August, of 11m bbl, thanks to healthy declines in gasoline and distillate stocks. Crude production in the US rose, however, to 12.5m b/d, substantially more than Saudi Arabia’s total capacity of around 12m b/d. Exports from the US also moved back up above 3m b/d, more than the entire production capacity of Kuwait.

Edward Bell

Edward Bell