Recent Search

Popular Searches

.jpg?h=457&w=800&la=en&hash=16940B73C632BAB462B3B27F8966E882)

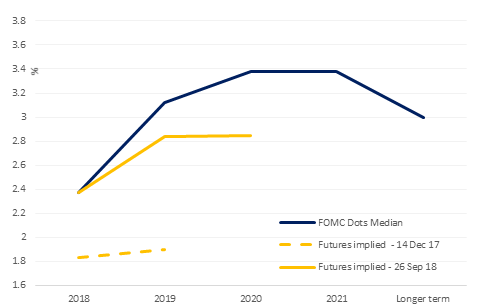

As anticipated, the US Federal Reserve raised rates by 25bps yesterday, taking the Fed target rate range to between 2.00% to 2.25%. The median projection of future rate hikes was left largely unchanged with slight increase in the long term neutral rate from 2.875% to 3%. The tone of the Fed’s statement was upbeat with upward revision of the GDP forecast for 2018 to 3.1% (previously 2.9%) and expectations of unemployment and inflation remaining near the Fed’s target ranges.

On the economic data front, New Home sales in the US rose 3.5% in August to 629k from a downwardly revised 608k in the prior month (previously estimated at 627k). The results matched consensus expectations, which called for an increase to 630k. The rise dovetails with an 11.6% surge in housing completions for the month, suggesting that strength in sales likely stems from the lack of available inventory.

Contrasting the optimism in the US, consumer confidence in France – the euro area’s second-largest economy, sank to the lowest level in more than two years in September. Overall confidence indicator fell to 94 from 96 in August. Households are more pessimistic about the outlook for their personal finances, think the standard of living has declined and there’s greater risk of unemployment.

JP Morgan yesterday confirmed that beginning Jan 31, 2019, sovereigns and quasi sovereign issuers from UAE, Saudi Arabia, Qatar, Bahrain and Kuwait will become eligible for inclusion in its widely followed, EMBI Global Diversified (EMBIGD), EMBI Global (EMBIG) as well as the Euro-EMBIG indices. Oman was already in the indices. Both conventional as well as sukuk are eligible for inclusion though sukuk would have to be rated. GCC issuers are expected to represents circa 11% of the indices and inclusion in the index is expected to support good bid for GCC bonds in the coming months.

Treasuries closed higher following the Fed meeting as there was little surprise from the Fed meeting. The Fed raised rates by 25 bps and signalled another increase in December 2018. Yields on the 2y UST, 5y UST and 10y UST closed at 2.81% (-2 bps), 2.94% (-4 bps) and 3.04% (-5 bps).

Regional bonds closed higher in line with moves in the UST. The YTW on the Bloomberg Barclays GCC Credit and High Yield index dropped -6bp to 4.45% and credit spreads remained flat at 160 bps.

Despite a 25 bps hike in interest rates from the Federal Reserve and more policy makers expecting a further increase in interest rates in December 2018 (12/16 compared to 8/16 at the last meeting), the dollar has failed to advance in the Asia session this morning. As we go to print, the Dollar Index (DXY) is unchanged, trading at 93.88.

Elsewhere, NZD is softer in the aftermath of the RBNZ interest rate decision and press conference. While the central bank kept interest rates at a record low of 1.75%, the statement was dovish in nature with Governor Adrian Orr stating that the interest rates would likely remain at this level into 2020. In addition, he communicated that while inflation was rising, risks to growth persisted and highlighted “trade tensions” between major global economies as a head wind. As we go to print, NZDUSD is trading 0.12% lower at 0.6655.

Developed market equities closed mixed as banking sector stocks closed lower in the US following the Fed meeting. The S&P 500 index lost -0.3% while the Euro Stoxx 600 index gained +0.3%.

UAE bourses closed higher with the DFM index and the ADX index adding +0.8% each. Elsewhere the Tadawul (-0.2%) closed lower on profit booking with Sabic dropping -1.4%.

Oil prices remain well bid in light of growing anxiety that the US sanctions on Iran will sharply disrupt oil markets. US energy secretary Rick Perry also added to the bullish tone by indicating the US would not release crude from its strategic petroleum reserve to compensate for the drop-off in Iranian production. Crude inventories built unexpectedly last week by more than 1.8m bbl as refineries sharply cut back on processing. Production did tick higher to 11.1m b/d last week. Both benchmarks are up around 1% so far this morning.

Click here to Download Full article