Recent Search

Popular Searches

One year on from the Russian invasion of Ukraine, the ramifications for the world economy are still very much to the fore. The surge in energy and food prices in the months following the outbreak of hostilities in Eastern Europe exacerbated the pandemic-related supply chain disruptions and pushed up global inflation sharply. While energy and food prices have since moderated, the second-round impacts on the costs of goods, services and wages have kept inflation elevated, forcing central banks to aggressively raise interest rates in the second half of last year.

The tightening in financial conditions on the back of rate hikes, as well as increased energy costs, have weighed on global growth, especially in Europe which was particularly dependent on Russia’s gas exports. While the Eurozone and the UK narrowly escaped a recession in the fourth quarter of 2022, most economists still expect a mild economic contraction or at best very weak growth for the major European economies this year.

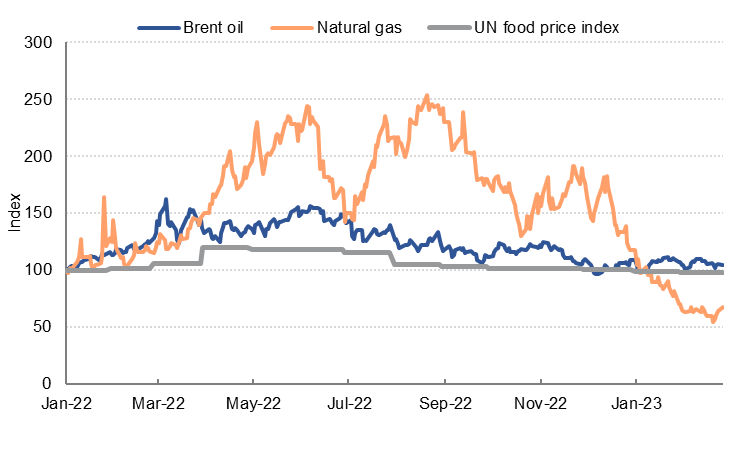

Oil prices have largely fallen back to pre-war levels as the market worries about weaker demand in developed economies. Natural gas prices have declined below January 2021 levels thanks to a milder than expected European winter. Food prices, measured by the UNFAO World Food Price Index are also down y/y in January 2023 and this should provide some relief to consumers and help to bring down headline inflation in the coming months.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

However, the relief on energy prices may be temporary. As China’s economic activity normalizes following the relaxation of zero-Covid policies, demand for energy from China is expected to rise significantly over the year. Meanwhile supply remains constrained by the lack of investment in capacity and - since the Ukraine war - sanctions on Russian energy exports. Emirates NBD expects oil prices to rise above USD 100 in the second half of this year, which will complicate central bank policy making as it implies inflation may start to accelerate at a time when many in the market expect the Fed to start cutting rates. Indeed, the economic data since the start of the year suggests that while headline inflation has slowed, the pace of decline may not be as quick as had been expected a couple of months ago, and central bankers are likely to remain hawkish for the time being.

The issue of energy security more broadly has also become more prominent in the wake of the war and is likely to have longer term consequences for investment. In response to EU sanctions, Russia reduced supplies of natural gas to Europe last year, pushing up prices and risking a shortage over the winter. The EU moved quickly to diversify their energy imports, securing new supplies of LNG but also launching a EUR 300bn program to increase renewable energy and to encourage greater efficiency in fuel usage. The shift towards non-hydrocarbon, alternative energy has become imperative, not just to tackle climate change but to ensure that economies have more secure and reliable energy supplies.

For the UAE and the rest of the GCC, the economic impact of the conflict in Europe has been more mixed. The UAE has seen interest rates rise by 450bp since the middle of last year as the Fed has hiked rates, and borrowing costs are now the highest since the financial crisis in 2008. This is likely to impact both consumer spending and private sector investment, with slower growth consequently expected in 2023.

However, governments in the region have benefitted from higher energy prices and increased exports which have allowed them to repair balance sheets after the pandemic, rebuild reserves, and push budgets into surplus. With oil prices expected to remain elevated this year, there is scope for increased public sector investment into infrastructure and other projects, which should support overall GDP growth.

A version of this article was published in The National on 24 February 2023.

Khatija Haque

Khatija Haque