Recent Search

Popular Searches

Kuwait’s long-ruling Emir Sheikh Sabah Al Ahmed passed away yesterday at the age of 91. The cabinet confirmed that Crown Prince Sheikh Nawaf Al Ahmed, the late Emir’s half-brother, will succeed him as ruler and will be sworn in on Wednesday. Sheikh Nawaf is 83 years old and is not expected to make any significant policy changes. A new crown prince will need to be announced and approved by a majority in the National Assembly. Separately, parliament approved a long-awaited insolvency law yesterday which should help to attract foreign investment, but is yet to approve legislation that would allow the country to issue external debt to finance a widening budget deficit this year.

Economic sentiment in the Eurozone managed to eke out a fifth consecutive month of stronger readings, as the European Commission’s survey rose to 91.1 in September, up from 87.5 the previous month and the nadir of 64.9 hit at the peak of the lockdown in April. Nevertheless, the rebound is slowing, and as ECB President Christine Lagarde noted this week, the risks are to the downside as Covid-19 cases surge once more. According to the survey, the services sector saw a greater improvement than manufacturing, but this trend is unlikely to hold as a larger share of the bloc’s population comes back under restrictions on movement and activity. The consumer sentiment index rose to -13.9 from -14.7, but this too is likely to come under pressure in the next survey.

China’s official PMI figures indicated that the economy continues to strengthen, with both the manufacturing (51.5, compared to consensus predictions of 51.3) and non-manufacturing (55.9 compared to 54.7) exceeded expectations and the previous month’s print. The Caixin manufacturing PMI came in just under expectations at 53.0 compared to 53.1.

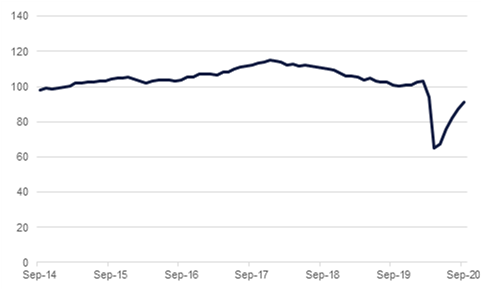

In the UK, mortgage approvals in August rose to a 13-year high, bolstered by pent-up demand over the lockdown period and the stamp duty holiday introduced by the Conservative government, which raised the threshold for paying taxes on property purchases to GBP 500,000. However, the August spike does not fully offset the dip in approvals through lockdown, while the August increase in consumer credit missed expectations, suggesting that many in the UK remain wary of the future.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

US treasury markets continued to linger in the range they’ve held to for much of the past few weeks, likely waiting for the outcome of the first US presidential debate to establish a candidate with a clear leader in the polls. Yields on 2yr USTs settled at 0.123% while on the 10yr they closed at 0.6495%, far less than 1bp lower than a day earlier. European bond markets were a bit more active with yields down across the board as calls mount for more ECB stimulus: yields on 10yr bunds closed lower by almost 2bps while gilt yields close down by 2bps.

Egypt issued the first sovereign green bond in MENA overnight with a coupon of 5.25%, tighter than initially proposed, and raising USD 750m with a considerable order book. Green bonds have a tendency to price at lower yields and can attract a growing pool of ESG-oriented investors.

The dollar remained on the defensive on Tuesday. The DXY index declined by -0.4%, falling below the 94 handle to reach 93.840. A break towards the 50-day moving average of 93.306 is within reach. USDJPY consolidated minor gains but is little changed from last week's closing price at 105.61.

The EUR was amongst the biggest movers, advancing by 0.67% to trade at 1.1744. A gauge of the region's economic confidence improved slightly in September but a recent resurgence in virus infections has cast uncertainty over the outlook. GBP has oscillated overnight and into trading today as concerns about Brexit weigh on the currency as it has retreated from highs of over 1.29 in the evening. Both the AUD and the NZD advanced for a second session in a row but have started to dip early this morning. Nevertheless the currencies have recorded modest gains since Monday's closing price to reach 0.7115 and 0.6590 respectively.

Most global equity indices closed in the red yesterday, although trading was largely fairly subdued ahead of the first presidential debate last night. In the US, the NASDAQ lost -0.3% while both the Dow Jones and the S&P 500 closed -0.5% lower. Europe was a similar story, with the CAC, the DAX and the FTSE 100 losing -0.2%, -0.4% and -0.5% respectively, with a number of earnings warnings weighing on UK shares. Asian indices are trading higher this morning, as the fairly positive PMI figures lead to a 0.6% gain on the Shanghai Composite and 1.8% on the Hang Seng at the time of writing. Chinese markets will close for a week tomorrow.

Within the region, the Boursa Kuwait closed down -2.2%, while the DFM and the Tadawul lost -0.4% and -0.6%.

Oil prices fell sharply overnight with both Brent and WTI futures down by around 3.3%. Brent settled at USD 41.03/b and is now trading back with a USD 40/b handle while WTI closed at USD 39.29/b and is hovering just above USD 39/b at the moment. Markets likely took little heed from the US presidential debate as there were few new elements related to energy or climate policy announced by either candidate.

The API reported a draw of crude stocks of 831k bbl last week but a build in gasoline. Official data from the EIA will be released later this evening.

Daniel Richards

Daniel Richards