Recent Search

Popular Searches

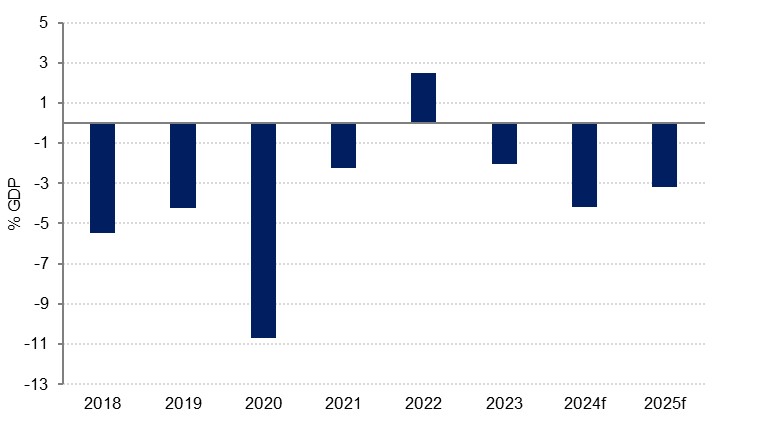

Saudi Arabia has reported a budget deficit of SAR 80.1bn for 2023, equivalent to 2.1% of GDP. This is moderately wider than the 1.9% shortfall we had forecast and stands in contrast to the 2.5% surplus seen in 2022, which was the first positive balance since 2013.

The key variable between 2022 and 2023 was in the oil sector, with last year seeing both lower average prices and lower output as OPEC+ members, and Saudi Arabia in particular, curbed production as they looked to put a floor under prices. Brent futures averaged USD 82.2/b last year, down 16.9% from 2022, while at 9.6mn b/d, Saudi’s oil output was down 8.6%, leading to a 12.0% fall in oil revenues to SAR 754bn.

Source: Haver Analytics, Emirates NBD Research

Source: Haver Analytics, Emirates NBD Research

By contrast, non-oil revenues rose 11.4% last year to a new record of SAR 457.7bn, in further evidence of the robust expansion in the non-oil sector. While there has been an ongoing diversification of government revenues in recent years, oil revenues still account for the bulk of income (62% in 2023), leaving total revenues down 4.4% in 2023. (Oil revenues as a percentage of total income have fallen from an average of 89% over the decade to 2013, to 66% over the past 10 years). Breaking down non-oil revenues, tax on goods and services was up 4.4%, while investment income rose 15.1%. The third largest component, tax on income, profit, CGT grew 57.8%.

On the expenditure side, total expenditure was up 11.1% last year. Current expenditure rose 8.4%, slightly slower than the 10.8% growth in 2022. Within that, spending on wages and salaries was up 4.7%, while goods and services spending rose 17.5% and social benefits spending was 22.1% higher. Capital expenditure spending accelerated to 30.0%, up from 22.4% the previous year, as the government ploughed ahead with its diversification programme and related expenditure. In terms of sectoral spending, the military remained the largest component despite falling 5.1% over the year.

Deficit will widen in 2024

This year we anticipate that the budget deficit will widen further, to around -4.2% of GDP, as spending commitments remain even as oil production curbs continue. Our forecast for oil prices is broadly similar to last year, predicting Brent futures to average USD 82.5/b, while with oil production curbs remaining in place through the first quarter at least, we expect Saudi Arabian oil output to fall to an average 9.2mn b/d for 2024. The forecast decline in oil revenues will be partly offset growth in non-oil income as other sectors continue to growth in importance.

While we expect government spending growth in KSA to slow this year, we do not anticipate an outright decline in spending. In October, the Saudi Arabian government revised its budget forecasts for the next several years, committing to budget deficits where previously it had envisaged surpluses as the government remains committed to ‘funding and supporting the implementation of programs, initiatives, and economic transformation projects in line with Saudi Vision 2030.’ Finance minister Mohammed al-Jadaan has acknowledged that some of the Vision 2030 projects could be extended beyond the present deadline, but with some major upcoming sporting events requiring significant investment in stadia and other related infrastructure within a short timeframe, there are limits on what can be delayed.

Debt will finance deficit

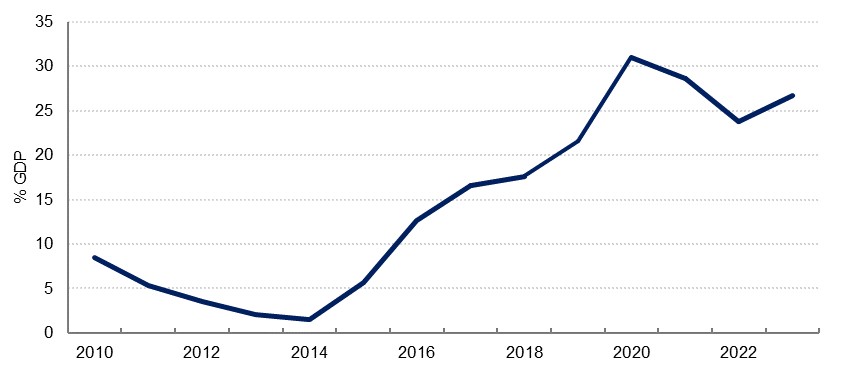

The bulk of the budget deficit was financed by public borrowing last year, with government debt rising to SAR 1.05tn, or 26.7% of GDP. This was up from SAR 990.1bn, with the SAR 60.2bn rise in public sector debt representing 74.4% of the budget shortfall. The borrowing last year was fairly evenly split between internal and external debt issuance, but at SAR 644.4bn, or 61.4%, domestic debt still comprises the greater share of the total debt stock. Public debt remains fairly low by international standards and we anticipate that the government will continue to tap both domestic and international debt markets over the next several years in order to fund the projected budget deficits. In January, the government issued USD 12bn in bonds, its largest since 2017, as it took advantage of lower yields.

Daniel Richards

Daniel Richards