Recent Search

Popular Searches

.jpg?h=457&w=800&la=en&hash=4FB1B3565A139724D40B0790B7FEBFEB)

US President Trump and Jean-Claude Juncker, the president of the European Commission have agreed to suspend the imposition of any new tariffs following Juncker’s trip to Washington while the two parties negotiate over their respective trade terms. The EU has pledged to import more LNG and soybeans from the US and that tariffs in general will be lowered – though not yet those on autos. There was also an agreement that tariffs already introduced on steel and aluminum earlier in the year will be reexamined, though they will remain in place for now. While there remain key stumbling blocks, the outcome of the visit was more positive than many expected, and will be particularly reassuring to the autos sectors on both sides of the Atlantic. Ford announced yesterday that the extra tariffs had added USD 145mn to its North American costs in the first half of the year as it cut its earnings forecast.

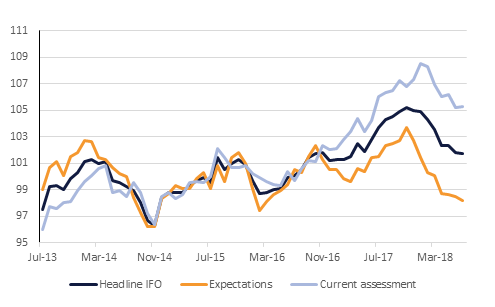

The results of Germany’s IFO business survey for July were released yesterday, with the headline figure of 101.7 beating consensus estimates of 101.5 and down only marginally on the 101.8 recorded in June. The current assessment component was at 105.3, but the expectations component was far weaker at 98.2. The threat of more tariffs is a likely reason behind the disparity, and manufacturers showed a greater decline in confidence than firms involved in services. Although Germany’s IFO index has fallen to the lowest level since March 2017, it remains far above long-run averages and the ECB is unlikely to deviate from its line that growth is healthy enough to warrant a gradual normalisation of monetary policy following its meeting today. While no meaningful change to the previously announced plan of ending its bond-purchase programme this year and raising interest rates in 2019 is expected, investors will be looking for clarification on the definition of summer in the sentence ‘The Governing Council expects the key ECB interest rates to remain at their present levels at least through the summer of 2019.’

There has been a delay to the results of the Pakistani general election being announced, owing to technical difficulties. Challenger Imran Khan’s Movement for Justice appears to be leading, though a hung parliament is the most likely outcome. This would entail a period of horse trading and prolonged uncertainty for investors.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

Treasuries closed higher amid strong auction demand and late strength in US equities. Yields on the 2y UST, 5y UST and 10y UST closed at 2.66% (flat), 2.84% (-1 bp) and 2.96% (-1 bp) respectively.

Regional bonds closed higher even as it continued to trade in a tight range. The YTW on the Bloomberg Barclays GCC Credit and High Yield index dropped -4 bps to 4.43% and credit spreads tightened -3 bps to 167 bps.

In terms of rating action, Moody’s affirmed the Ba2 corporate family rating of Dubai Aerospace Enterprise and Ba3 senior unsecured rating of DAE Funding LLC and revised the outlook to positive from stable.

The EUR has recovered back above 1.17 following comments from President Trump saying that he has secured an agreement with the EU to avoid a trade war. Europe is reportedly agreeing to lowering industrial tariffs and import more U.S. soybeans. However, the CNY has reversed earlier gains suggesting that China is likely to remain in the cross hairs over trade with few expectations that China’s dispute with the US will be resolved as easily. Meanwhile the USDJPY rate remains heavy as the markets continue to speculate that the BOJ may adjust its loose monetary policy at its meeting next week.

Developed market equities closed mixed as the European Union and the US reached an agreement to avoid a full-blown trade war. The announcement came after the close of European markets. The S&P 500 index and the Euro Stoxx 600 index closed +0.9% and -0.3% respectively. Facebook declined as much as -24% in aftermarket trading as the company’s revenues came in below expectations and the company warned of further slowdown in growth in Q3 and Q4 2018.

UAE bourses outperformed their regional peers with the DFM index and the ADX index adding +0.7% and +1.1% respectively. First Abu Dhabi Bank added +2.6% after reporting better than expected Q2 2018 earnings.

Brent futures closed up 0.7% overnight, at USD 73.93/USD, while WTI gained 1.1% to USD 69.30/USD. The probable driver was the inventories data release from the EIA last night which showed that US crude stockpiles have fallen to three-year lows. Another likely factor was a temporary suspension in Saudi shipments through the Bab el-Mandeb after two oil tankers were attacked by Houthi militia members.

Daniel Richards

Daniel Richards