Recent Search

Popular Searches

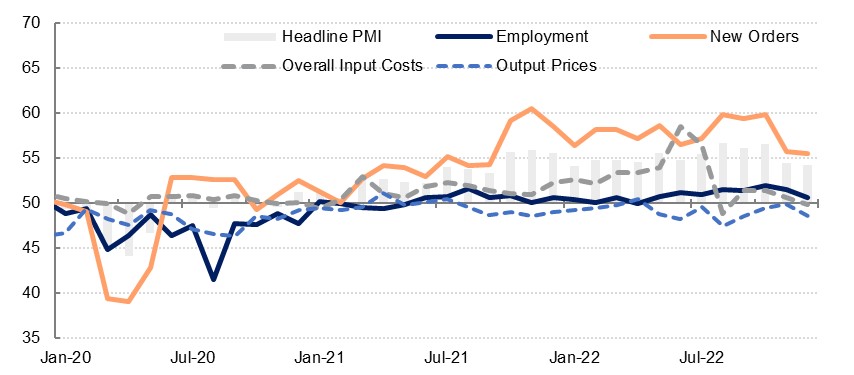

The S&P Global PMI survey for the UAE confirmed a slowdown in growth momentum in Q4 2022, after a strong third quarter. The headline index fell to 54.2 in December from 54.4 in November and 56.6 in October. While business activity and new orders increased last month, they grew at the slowest pace since September 2021. New export orders declined slightly last month, reflecting weaker external demand.

Source: S&P Global, Emirates NBD Research

Source: S&P Global, Emirates NBD Research

Private sector firms slowed hiring in December and staff costs were unchanged. Purchasing activity also slowed even as input costs slipped slightly. We expect further relief on input costs in January as the petrol price was cut by 16% m/m this month. Firms passed on some of their lower costs to consumers, with selling prices falling at the fastest rate in three months.

While firms were somewhat optimistic about the outlook over the next year, the future output index declined to its lowest level since February 2021 as firms fretted about the deteriorating global backdrop and what this could mean for their business activity in 2023. We expect non-oil sector growth to slow to 3.5% in the UAE this year from an estimated 5.6% in 2022.

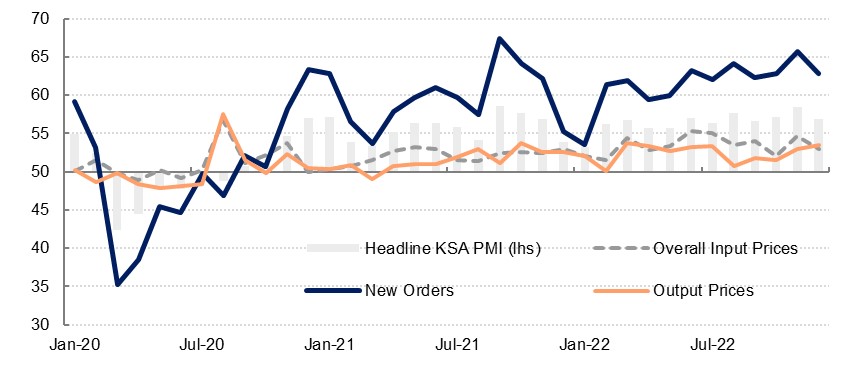

The Riyad Bank PMI for Saudi Arabia slipped to 56.9 in December from 58.5 in November. New order growth and business activity remained robust, but these sub-indices declined slightly from last month. New export orders also rose at a slower pace in December.

Source: S&P Global, Emirates NBD Research

Source: S&P Global, Emirates NBD Research

Firms in the non-oil sector increased hiring at the fastest rate in almost five years, as business activity rose sharply through 2022 and optimism about future output remained relatively high. Staff costs also increased modestly. Overall input cost inflation slowed from November however, but firms still raised selling prices on average at the fastest rate since March 2022.

Despite overall optimism about the outlook for the next year, firms slowed their purchasing activity in December, and the stocks of pre-production inventory increased at the slowest pace since September 2020.

Notwithstanding the modest softening in activity at the end of 2022, we expect Saudi Arabia’s non-oil sector to grow 4.5% in 2023, underpinned by strong domestic demand and public sector investment. Government capital spending via the budget rose by 29% in 2022 and is expected to increase by a further 4% in 2023.

Egypt’s PMI survey from S&P Global improved in December, rising to 47.2 on the headline reading from 45.4 the previous month. While this still indicates a contraction in the private sector economy, it is at a more sedate pace as compared to November, which was the first reading post the new IMF deal and the move lower by the Egyptian pound at the end of October.

Output improved modestly in December from November but remained below the neutral 50.0 level as high prices constrained business. New orders also declined at a slower pace, with domestic business seemingly accounting for the contraction: new export orders expanded for the first time since July 2022, albeit marginally, likely benefitting from the cheaper EGP.

Costs rose sharply again in December, but this was also slower than seen in November and was only marginally faster than the October reading. The rise in overall input prices has been driven largely by the increase in purchase costs following the pound’s depreciation (alongside other global factors), as staff costs rose far more slowly. Output price inflation slowed slightly in December but remains high as businesses try to pass on some of their higher costs to consumers. This will likely keep CPI inflation – 18.7% y/y in November – elevated in the coming months.

Businesses also looked to maintain their margins through cutting staff numbers as workloads fell, and by cutting their purchases, which fell at the fastest pace in six months and marked a 12th consecutive contraction. Business optimism improved in December but it remains low compared with the series average. Some 15% of respondents expect conditions to improve in 2023 while only 1% expect a decline in activity.

Daniel Richards

Daniel Richards