Recent Search

Popular Searches

Nonfarm payrolls data in the US showed that 312k new jobs were added in December, far above market estimates and the second largest increase in 2018 as a whole. The growth was broad based. As a whole, more than 2.6m jobs were created in 2018 compared with 2.2m in 2017. Average hourly earnings in December rose 3.2% y/y while the unemployment rate rose to 3.9% mainly due to increased labour force participation. The report validated the fact that while manufacturing and housing data may be showing some signs of slowing, the labour market in the US remains buoyant.

Despite the strong NFP report, Fed Chair Jerome Powell gave a more cautious statement at the end of the week, perhaps in an effort to address some of the downward moves in financial markets over the last month. Powell indicated that the Fed would be ‘patient’ in assessing economic conditions and that the central bank was prepared to shift policy ‘significantly’ if warranted. Equity markets soared on the back of Powell’s commentary—the S&P 500 gained more than 3.4% on Friday—on the implication that the trajectory for rates in 2019 may not be as steep as initially feared.

The People’s Bank of China (PBOC) announced 100bps cut in Required Reserve Ratio (RRR) for banks, including 50bps effective 15 January and another 50bps effective 25th January. The move is expected to free up estimated liquidity of around RM800bn and is in response to increasing downside risks for China’s economic growth from external trade conflict, slowing housing market and softening consumption. The RRR cut is seen as a credible signal that the Chinese government is committed to maintaining stable economic growth and containing systemic risks.

Growth in Japan’s services and manufacturing sectors slowed in December. The Markit/Nikkei Japan Services PMI came in at 51 in December vs 52.3 in November and the Composite PMI reduced to 52 from 52.4 in November. That said, the readings are not too far from the 51.1 and 52.2 respectively recorded an year ago. Sales tax in Japan is set to increase from 8% to 10% in October this year which is making policy makers worry about a fall in consumer spending.

Strong NFP data pushed UST yields higher over the weekend. However even with 12bps increase in 2yr UST yields to 2.49%, they remain below the previous week’s close of 2.52% and well below the highs of 2.97% reached in mid-November. Yield on 5yr and 10yr USTs also closed higher on the day at 2.50% and 2.67% respectively though lower by -5bps each over the previous week.

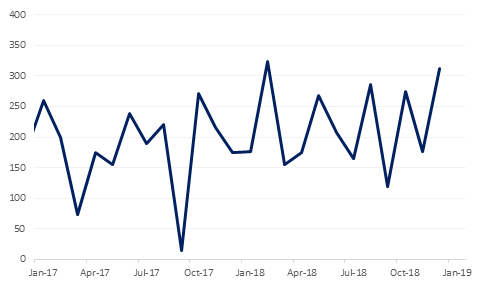

Locally GCC bonds followed suit with benchmark yield movements. Yield on Barclays Bloomberg GCC bond index closed the year at 4.66% (+93bps y/y) and currently running at around 4.63%. Credit spreads at around 210bps are at its highest level in over two and half years.

Last week’s 0.42% decline saw EURUSD close at 1.1396, down from the one month highs of 1.1497 seen on the 2nd of January in line with our Q4 2018 forecast of 1.15. Of note is that over the course of the week, the 100-day moving average (1.1479) continued to provide resistance, while the 50-day moving average (1.1370) provided support. Analysis of the weekly candle chart shows that for a tenth week, the 200-week moving average (1.1317) halted additional losses for the cross and while this continues to provide support, we expect a retest of the 1.15 level.

Despite falling as low as 1.2441 (the lowest level since April 2017) from its opening of 1.2699, GBPUSD was able to recover and actually finished the week 0.19% higher at 1.2724. Despite three weeks of gains, the price remains below the technically significant 100-week moving average for a twelfth week and as a result and the downtrend remains intact. The 14-day Relative Strength Indicator (RSI) is bullish in momentum, but gains may be limited by resistance at the 50-day moving average (1.2772), a level which has capped gains since November 2018.

Regional equities started the week on a positive note. The Tadawul was led higher by Al Rajhi Bank after the bank announced 7 bonus shares for every 13 held and proposed H2 2018 dividend of SAR 2.25 per share.

Oil markets began the year on a positive footing, gaining three days in a row to start 2019. Brent futures rose 9.3% to end the week above USD 57/b while WTI added 5.8% over a holiday-shortened week of trading to close just shy of USD 48/b.

OPEC’s new production cuts have taken effect from the start of the year and market surveys of OPEC output show that major producers got started early. Collective OPEC production fell by 630k b/d in December according to Reuters estimates with Saudi Arabia seeing a decline of 400k b/d and the UAE falling by 110k b/d.

Contango structures narrowed a little in the first week of the year, helped by the rally in front-month prices. Time spreads at the front of the Brent curve closed at a contango of USD 0.15/b while WTI levelled off at USD 0.32/b.