Recent Search

Popular Searches

.jpg?h=600&w=800&la=en&hash=809484D1CEB865C9E4BEB3CAFBF462A8)

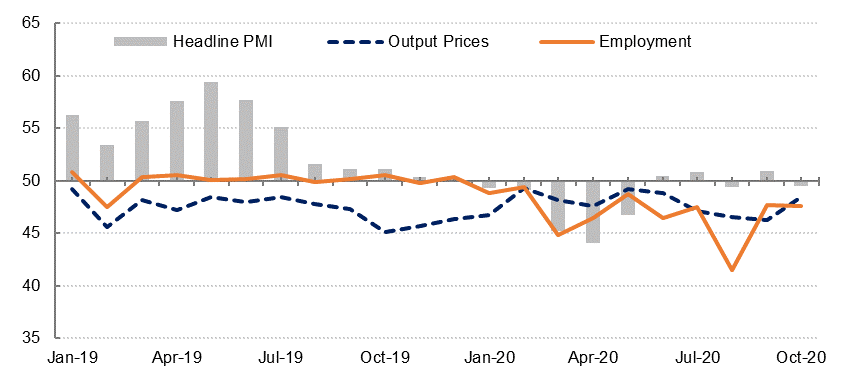

The UAE’s headline PMI slipped below the neutral 50-level in October, for the second time in three months, declining to 49.5 from 51.0 in September. Output growth slowed while new orders declined for the first time since May. Firms remained concerned about the impact of the coronavirus pandemic on activity and spending over the next twelve months, with the “future output” index declining to a series-low of 51.7. With a focus still on curbing costs in the face of soft demand, businesses in the private sector again reduced headcount in October, at a similar rate to September.

Backlogs of work declined at the fastest rate since 2011, and there is little evidence of producer price inflation, indicating excess capacity in the private sector. Firms again discounted selling prices to support demand, but the extent of price discounting was weaker than in the prior three months.

The UAE PMI has averaged 50.2 since June, when lockdown restrictions were eased. While the survey data indicates a modest recovery in output over the summer, output likely remains well below pre-Covid19 levels. Moreover, the external outlook has deteriorated in recent weeks: a surge in coronavirus cases has led to extensive lockdowns being re-imposed across Europe (including the UK) and tighter restrictions on travel, while the lack of additional fiscal stimulus in the US is a further headwind to growth in Q4 2020. A Covid-19 vaccine has yet to be approved even for emergency use in Europe or the US, and this is looking less likely to happen before 2021, later than we had anticipated.

In light of the relatively soft regional PMI data in recent months, and the weaker external backdrop for Q4 2020, we have revised down our 2020 UAE GDP growth forecast to -6.9% from -5.5% previously. However, we have revised our 2021 growth forecast up to 1.9% from 1.2% previously.

Source: IHS Markit, Emirates NBD Research

Source: IHS Markit, Emirates NBD Research

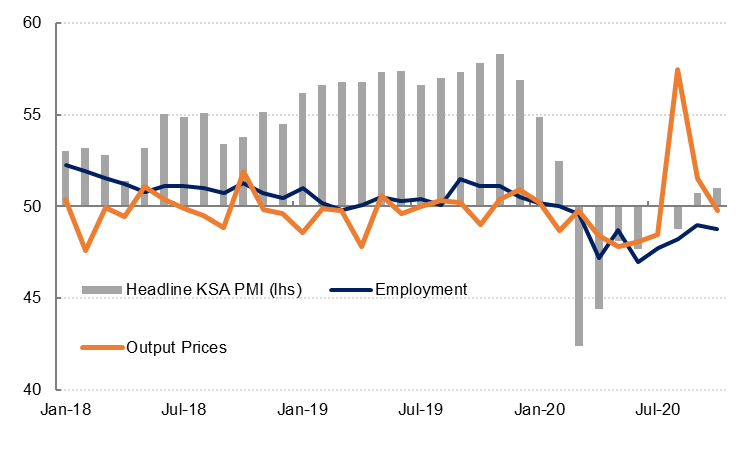

Saudi Arabia’s PMI rose to 51.0 in October from 50.7 in September, signaling a gradual recovery in non-oil private sector business conditions. Private sector output increased at the fastest rate since February, but at 52.9 this index remains well below the series average 61.7. New order growth slowed in October as new export orders declined.

Despite the increase in output, private sector firms shed jobs in October for the eighth month in a row. Input costs increased modestly from September, but firms kept selling prices largely unchanged, citing strong market competition.

Firms remained broadly optimistic about the next twelve months, but the degree of optimism was softer than in September as some firms cited high uncertainty about the outlook. We retain our -5.2% GDP forecast for KSA in 2020, and we expect growth to recover to 3.3% next year.

Source: IHS Markit, Emirates NBD Research

Source: IHS Markit, Emirates NBD Research

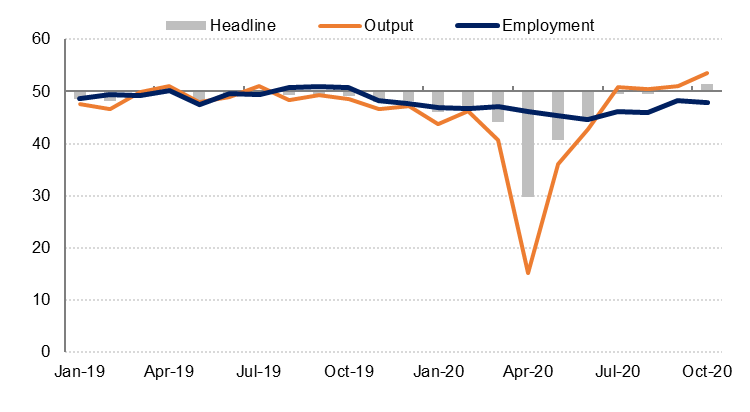

Egypt’s headline PMI rose to 51.4 in October from 50.4 in September, the highest reading since December 2014. Output and new orders increased at a faster rate in October, and firms also increased their stocks of inventories which contributed to the higher headline index. However, employment in the private sector declined again last month.

Selling prices increased in October as firms passed on higher purchase costs to customers. Overall, businesses remained optimistic about the outlook over the next twelve months, although the future output index declined to 62.0 from 66.3 in September.

Source: IHS Markit, Emirates NBD Research

Source: IHS Markit, Emirates NBD Research

Khatija Haque

Khatija Haque