Recent Search

Popular Searches

On the one-year anniversary of the Trump presidency, the U.S. government officially shut down at midnight Friday after the Senate failed to secure enough votes to move forward on a four-week Continuing Resolution that was passed earlier last week by the House. The vote, which required the support of 60 senators to pass, fell largely along party lines with 50 votes in favour, and 49 votes against, with opponents of the bill unwilling to endorse it unless there was also a deal for ‘Dreamers’, or those protected under the Deferred Action for Childhood Arrivals (DACA) program, which was repealed by Trump last autumn. Tangible effects from the federal shutdown could be wide ranging, affecting government employees and facilities across the country that are deemed ‘inessential’. The 2013 shutdown saw as many as 850,000 workers furloughed per day, or about 40 percent of the federal workforce.

The economic damage will largely depend on how long the shutdown lasts, which in 2013 was only seventeen days. A stop-gap spending bill may be voted on as early as Monday that would keep the government open for three more weeks, but without resolving the wider issues over immigration. However, Democrats appear to be opposed to this and the biggest question mark about how to resolve the shutdown is President Trump himself who has offered inconsistent messages over his approach to the immigration issue.

Saudi Arabia’s energy minister has spoken in favour of keeping OPEC’s current production cuts in place beyond their scheduled expiry in December this year. Khalid al Falih spoke on the side of an OPEC monitoring meeting taking place in Oman to assess the effectiveness of the cuts. Falih’s comments come at odds with market anticipation that the deal may end early considering how high oil prices have risen. However, oil ministers from the GCC have been consistent in the messaging that no change in the scale of the cuts is currently required.

Source: Emirates NBD Research

Source: Emirates NBD Research

Strong economic data and the standoff over a US Government shutdown caused a steepening of the US treasuries curve last week which received further technical support from a fall in year-end demand recorded in December for longer dated treasuries from pension funds. Yields on 2yr, 5yr and 10yr treasuries closed at 2.06% (+7bps), 2.45% (+10bps) and 2.66% (+11bps) respectively. In contrast, government bonds in the UK recorded lower yields on shorter dated bonds and stable to only marginal increase in longer dated bonds. Yields on 10yr Gilts closed at 1.34% (+2bps). Subdued December inflation (core at only 0.9% y/y) in the Eurozone caused 10yr Bund yields to closed lower at 0.56% (-2bps).

Oil declining somewhat from its peak of over USD 70/b had little impact on appetite for credit risk. CDS levels on US IG and Euro Main closed lower by half a bp each during the week to 48bps and 45bps respectively while average option adjusted spread on global credit index was lower by a bp to 83bps.

Regionally, GCC Bonds had a week of weak trading as prices retreated in line with increasing benchmark yields. Average yield on Barclays GCC bond index increased 4bps to 3.73%, partly counter balanced by a decline in credit spreads by three bps to 125bps. S&P affirmed Ras Al Khaima’s rating at A with stable outlook. RAKS 25s have largely traded in sync with macro market moves, closing the week with yield at 3.36% (+4bps).

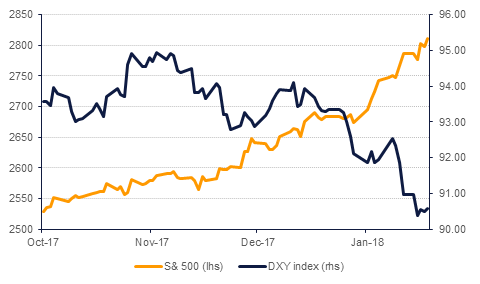

The Dollar Index continued its longest weekly losing streak since February 2017, falling 0.31% last week to close at 90.69. In the process, the index reached new 2018 lows of 90.11, a level not seen since December 2014. Technical analysis of the weekly candle chart shows the weekly downtrend that has been in effect since 30 December 2016 remains intact with a pattern of lower highs and lower lows being the prominent pattern. It is also noteworthy that the index has once again ended the week below the 200 week moving average for a fifth time and as well as broken below the supporting baseline which had held since June 2015. While the index trades below this key level, a possible decline towards 88.42 (the 38.2% five year Fibonacci retracement) remains a realistic scenario.

Regional equities made a negative start to the week following weak corporate newsflow. The Tadawul and the DFM index dropped -0.3% and -0.5% respectively. Almarai dropped 1.2% after the company reported a decline in Q4 2017 earnings. Union Properties gained 0.4% after the company confirmed that it sold its entire stake in Emicool to Dubai Investments for AED 500mn.

Oil prices fell last week, their first loss in 2018 and first weekly decline in the last five weeks. Brent futures fell 1.8% over the week to close at USD 68.61/b while WTI declined 1.4% to close at USD 63.37/b. The IEA kept its forecast for a slowdown in global demand growth in 2018, expecting 1.3m b/d this year from 1.6m b/d last year while it anticipates that non-OPEC supply will grow by 1.7m b/d this year. In the IEA’s estimation, if OPEC sticks to its deal with good compliance it will help ensure that the oil market moves close to balance this year. In the US, the drilling rig count dropped by 5 rigs last week and the overall count remains flat at around 750 rigs.

Market structures continue to weaken over the course of last week. The backwardation in 1-2 month spreads for both WTI and Brent softened. In WTI the backwardation is at just USD 0.06/b while in Brent it has settled back below USD 0.50/b. Investor positioning in Brent markets also fell last week thanks to some profit taking. However, it is still hovering near historically elevated levels.

Edward Bell

Edward Bell