Recent Search

Popular Searches

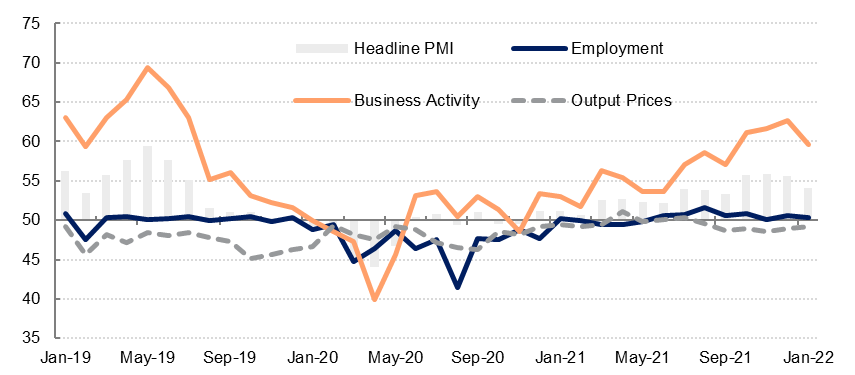

The UAE’s purchasing managers’ index (PMI) slipped to 54.1 in January from 55.6 in December, the lowest reading since September 2021. The survey still points to an improvement in business conditions in the UAE last month, albeit at a slower pace. Business activity increased sharply again in January, supported by solid new order growth. However, the rise in new coronavirus cases linked to the Omicron variant weighed on consumer spending and new export orders last month.

Source: IHS Markit, Emirates NBD Research

Source: IHS Markit, Emirates NBD Research

Input costs rose for the 12th consecutive month, and at a slightly faster rate than in December, reflecting higher costs of raw materials and transport. Firms have not been able to pass on these higher costs to buyers, with average selling prices declining for the last six months. With margins under pressure, firms have been reluctant to boost hiring in line with the growth in activity in recent months. While private sector employment has increased m/m since June 2021, the rate of growth has been weak.

Firms remain broadly optimistic about the outlook over the coming year, and while we expect the impact of the Omicron variant to weigh on Q1 growth, the UAE economy will likely continue to recover from the pandemic over the course of the year.

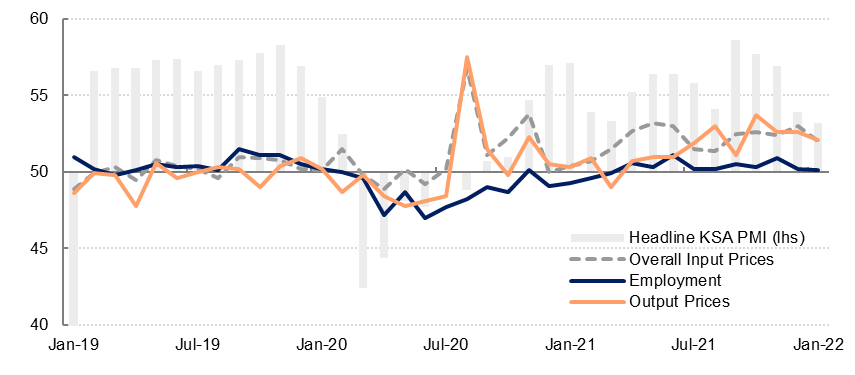

The Saudi Arabia PMI declined to 53.2 in January from 53.9 in December, indicating softer improvement in business conditions in the kingdom last month. The January PMI was the lowest since October 2020. Business activity and new order growth slowed, while new export orders declined for the first time since March 2021, as the spread of the Omicron variant weighed on both domestic and foreign demand.

As in the UAE, private sector firms in KSA reported higher input costs in January, but unlike in the UAE, firms in Saudi Arabia have been able to pass on most of these higher purchase costs to buyers. Selling prices have increased broadly in-line with input costs in recent months.

Firms remained cautiously optimistic about the outlook over the coming months, with the degree of optimism slightly higher than in December. High oil prices are likely to support business confidence in the near term as well, in our view.

Source: IHS Markit, Emirates NBD Research

Source: IHS Markit, Emirates NBD Research

There was a broad deterioration in business conditions in Egypt in January, as evidenced by the latest PMI survey. The headline index reading dropped to 47.9, compared with 49.0 the previous month, moving further into contractionary sub-50.0 territory. This was the weakest reading since April 2021 and marked the 14th consecutive month of contractionary readings. The spread of the Omicron variant of Covid-19, both at home and abroad, has weighed on activity, as have the ongoing issues around supply chains and related inflationary pressures.

Output contracted at the fastest pace since mid-2020 in January as construction and wholesale & retail trade shrank, but services managed to expand. New orders also fell at the fastest pace since June 2020, with domestic orders seemingly leading this given that export orders recorded a positive expansion, albeit at a much slower pace than seen in December. Respondents to the survey continued to cite problems around shipping and higher prices as disrupting their external trade.

Input prices continue to push higher, although at a slightly less rapid rate than seen in November and December. This was driven by purchase prices with the ongoing pandemic disruptions continuing to drive up costs of raw materials and shipping. By contrast, staff prices dipped compared to the previous month, as firms seemingly looked to protect their shrinking margins – employment fell in January for the third month in a row, with the construction and manufacturing sectors reporting a drop in employment numbers.

Some firms continue to pass these price pressures on to their customers, but the pace of this has softened and only 4% of firms said that they had raised prices – the output prices subcomponent of the PMI survey was at the lowest level since July 2021 in January. This PMI print comes ahead of the Central Bank of Egypt’s first rates announcement of the year later today, and our expectation is that the MPC will opt to keep the benchmark overnight deposit rate on hold at 8.25%. While core inflation has been rising the headline figure has dropped back from the levels seen several months ago, and some of the imported inflationary pressures are likely to soften further in the January inflation print. With the headline figure well within the CBE’s target range we do not believe that it will look to hike rates until later in the year, should external monetary conditions make it more expedient.

Daniel Richards

Daniel Richards