Recent Search

Popular Searches

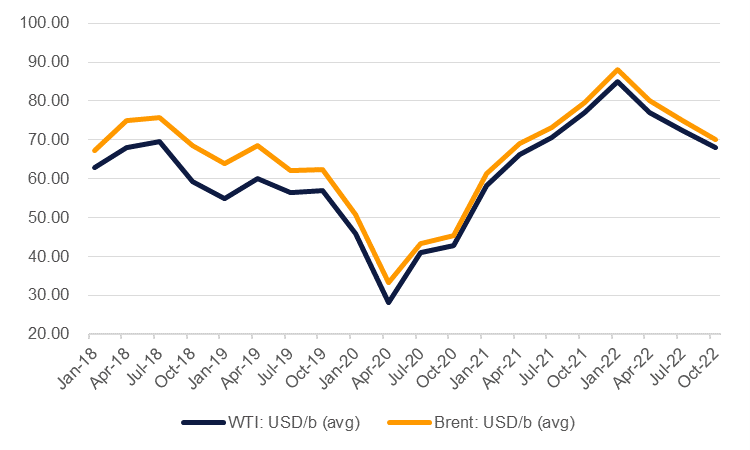

Oil prices have edged back from recent highs as press reports suggest a de-escalation of tensions in Eastern Europe with some Russian troops reportedly moving back to home bases upon completion of training exercises. Brent futures, which had moved up to nearly USD 97/b at the end of last week have moved to around USD 94/b.

The risk of a geopolitical incident continues nevertheless to hang over oil and energy markets. The UAE’s energy minister, Suhail al Mazrouei, suggested that prices are currently being driven more by geopolitics rather than fundamentals in commentary at an event earlier this week while the head of the International Energy Agency has likewise blamed the tensions for high spot prices. In that sense, oil prices at USD 90/b or more in the Brent market appear to already be pricing in an interruption to flows of Russian energy exports even though there has been no disruption of exports coming out of the country. Premiums for grades of Russian oil delivered to Asian markets have increased but have moved higher in line with the broader move upward in oil markets.

A tight balance in the first quarter

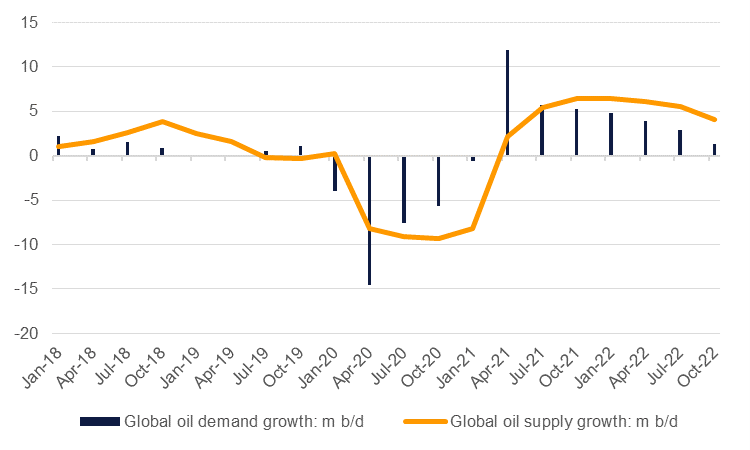

Oil markets do indeed appear tight for Q1 2022. Based on the IEA’s latest demand projections markets will be evenly balanced in the first few months of the year, supporting high prices. Over the rest of 2022, however, oil demand growth will flatten out from 4.8m b/d in Q1 to 1.4m b/d by Q4 as overall demand levels return to pre-pandemic levels. At the same time production is heading steadily higher. Projections for US supply growth this year range from around 800k b/d from the US government’s own EIA to more than 1m b/d from both OPEC and the IEA. Accompanied by higher output from producers like Canada and Brazil, non-OPEC+ production is set to increase by roughly 2m b/d this year.

Source: IEA, Emirates NBD Research

Source: IEA, Emirates NBD Research

OPEC+ too will add production this year, unwinding its pandemic-related cuts. So far, the producers’ bloc has been falling short of hitting its 400k b/d monthly supply additions as some exporters hit the limit of their production capacity. We had expected that Gulf producers within the OPEC+ alliance would restrain production short of their target levels to avoid over-supplying markets but so far that has not been the case; indeed, they have been some of the few producers who have managed regular monthly increases. Oil production from Saudi Arabia increased by 630k b/d between July 2021 and January 2022 while in the UAE production has risen to 2.91m b/d as of January, from 2.75m b/d when the plan to increase volumes was agreed in July last year.

OPEC+ will maintain supply increases

Our expectation now is that the OPEC+ countries that can hit their target levels will increase production, meaning upward revisions to our oil supply growth forecasts for Saudi Arabia, the UAE and a few others. So far there has been little movement from OPEC+ on making up the production shortfall from those that have missed targets and while we don’t think the producers’ bloc will endorse such a strategy there is nevertheless some upside risk to the supply outlook for the core Middle East OPEC countries.

Price outlook revised upward

Our initial projection for oil prices in Q1 2022 was for an average of USD 75/b on the Brent market and USD 72.50/b in WTI. Given the geopolitical risks in the market those levels now appear too low so we are marking our forecasts to market and revising our price targets higher. We now expect Brent at an average of USD 88/b in Q1 before moving lower over the remainder of the year, bringing the annual average to USD 78/b, up from closer to USD 70/b previously. For WTI we expect an average of USD 85/b in Q1 before following a similar trajectory to Brent and recording an average of USD 76/b for 2022, up from USD 67/b previously.

Source: Emirates NBD Research

Source: Emirates NBD Research

There are notable upside risks to this forecast. In the immediate term is the still unresolved geopolitical situation in Eastern Europe. Were a conflict to unfold then we would expect a sharp move higher in oil prices based on the assumption that Russian exports of energy commodities would be placed under sanctions. For the rest of the year upside risk relates to whether demand outperforms. China has yet to abandon its zero tolerance policy toward Covid-19 and any easing of restrictions there could mean more travel and industrial demand for energy.

Downside risks are present too. While there has yet to be any diplomatic breakthrough the prospect of the US and Iran returning to the terms of JCPOA could mean Iran is able to increase oil production by around 1m b/d by the end of the year. That would help keep oil market balances materially above balanced and deflate some of the high energy prices. Aggressive monetary tightening that prompts a severe slowing of activity in the US or other economies also represents a negative for oil prices over the course of 2022.

Edward Bell

Edward Bell