Recent Search

Popular Searches

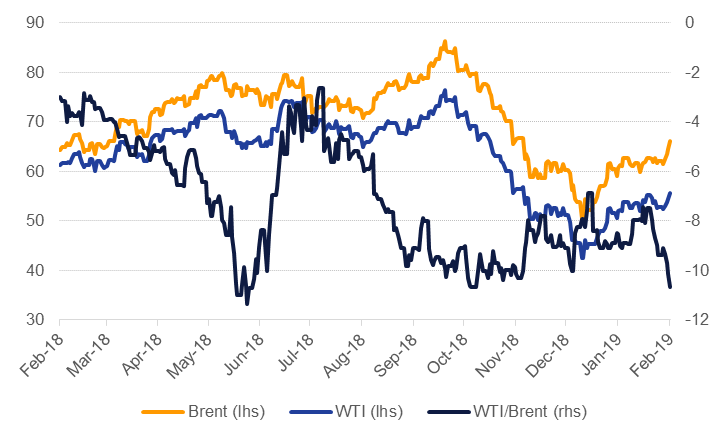

Both Brent and WTI futures extended their year-to-date gains last week and hit new high closes for the year. Brent added 6.7% last week to end at USD 66.25/b while WTI was up more than 5% to finish at USD 55.59/b. Risk assets generally performed well as markets expect an extension of the deadline on US-China trade talks, helping shore up sentiment amidst otherwise soft economic data. Several Fed officials have also indicated they are looking at fewer rate hikes this year than the central bank had projected earlier. A softer trajectory for the dollar will also help support crude prices near term.

The rally in oil markets was particularly striking as all the major forecasting agencies pointed to softening fundamentals in their latest market reports. OPEC cut its forecast for the call on its own members’ crude to 30.57m b/d thanks to higher output forecasts for non-OPEC supply growth (expecting growth of 2.18m b/d this year). The EIA revised its 2019 US supply forecast up sharply to 1.46m b/d from 1.14m b/d previously and also brought forward the date it expects the US to pass over 13m b/d of production to Q1 2020. Finally the IEA left its own demand forecasts unchanged while revising upward its non-OPEC supply forecast. Taken together, all the agencies pointed to a tight market for heavy, sour crude in H1 thanks to OPEC cuts and sanctions on PDVSA but none of them project a very positive outlook for other oil market indicators. Few economies are posting economic data outperformance and the US is now starting to show more signs of softening growth. Rising oil prices along with weaker economic growth is a trend with a short life expectancy that could unwind viciously in the oil market.

Brent time spreads, relatively more influenced by OPEC issues than WTI, tightened last week into a more consistent backwardation in the first two years of the curve. Dec spreads for 19/20 closed last week at over USD 1.5/b, more than doubling their level at the start of the week. Long-dated WTI spreads have also been tightening but at the front end of the curve, the glut of US oil is still weighing on spreads: a contango is still in play for the first nine months of the curve.

US exploration and development companies added another three rigs last week despite current WTI prices coming in close to break-even levels for many producers. Prices for Mars, a heavy grade of US crude from the Gulf of Mexico, remain elevated thanks to the relative tightness of heavy, sour crudes.

The gain in crude prices is providing little relief to refiners as margins continue to hover near year lows. A large weekly build in Singapore fuel oil and light distillate stocks helped push inventories there to their highest level since September 2017. Stocks in north-west Europe also edged higher while US crude stocks hit their highest level in the past year.

Source: EIKON, Emirates NBD Research.

Source: EIKON, Emirates NBD Research.

Edward Bell

Edward Bell