Recent Search

Popular Searches

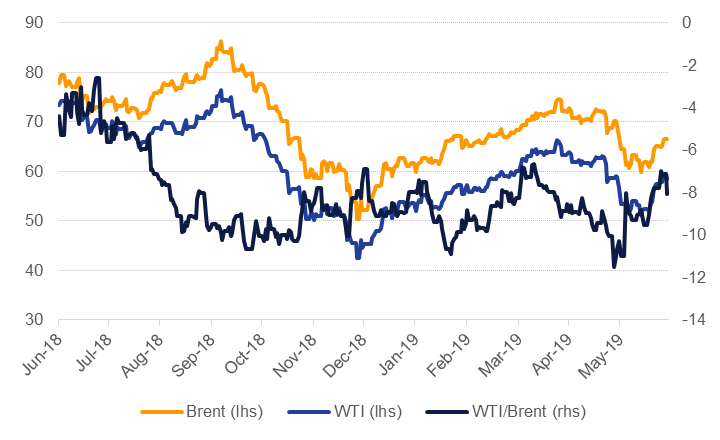

Oil markets ended the week higher and concluded a strong start to the first half of 2019. Front month Brent futures expired at the end of trading at USD 66.55/b, up 2% on the week and a gain of 21.2% year-to-date. Average prices in Q2 were USD 68.47/b compared with our forecast of USD 67.50/b. WTI futures gained 1.8% on the week, taking ytd gains to 28.8%. WTI hit an average of USD 59.91/b compared with our expectation of USD 57.50/b. As market focus turns to the next quarter, we maintain our forecasts for Brent to record an average of USD 67.50/b and WTI at USD 60/b.

OPEC meets this week with expectation that the production cut deal will be rolled over for at least the next six months of the year. The Russian president, Vladimir Putin, and Saudi Arabia’s crown prince, Mohammed bin Salman, have reportedly agreed on the side of the G20 meeting to an extension of between six to nine months and at current levels of 1.2m b/d. A roll-over of the production cuts into 2020 appears increasingly likely given a still strong supply growth picture outside of OPEC for next year. However, our expectation is still for output to increase from OPEC members that are unburdened by external factors (sanctions, civil conflict) over the next few months, even more now that security of supply has been shaken by rising geopolitical tension in the Gulf region. After the OPEC meeting concludes we will assess the market outlook for the rest of 2019 and 2020 in more detail.

Forward curves for both Brent and WTI have bounced off recent lows and December spreads for both benchmarks strengthened last week. Brent Dec 19/20 closed in a backwardation of USD 2.38/b while WTI was not far below USD 3/b for the same spread. The backwardation has been improving for both contracts but nevertheless still remains well off recent highs: Brent Dec 19/20 was over USD 4/b in the middle of May. Even with the escalation of geopolitical tension, the failure of spreads to recover past highs to us suggests that demand risks remain the dominant factor for markets at least for the next quarter. The G20 meeting over the weekend concluded with the US and China agreeing to restart trade talks but the risk of them falling apart, and weakening commodity demand further, still remains high. As a footnote to the impact the trade war is having, China’s official manufacturing PMI remained below 50 for June for a second month in a row.

Dubai spreads are displaying a particular insouciance to elevated geopolitical risks. Spreads in 1-3 months actually closed the week in a smaller backwardation (USD 0.93/b) and are substantially below 2019 highs of more than USD 2/b. Statements from ADNOC and Aramco officials that both companies will meet any demand from customers despite the risks to supply should serve to reinforce the message that crude volumes coming out of the Gulf region are unlikely to fall further. Official pricing may, however, edge lower given the relative weakness in Dubai spreads compared with other benchmarks.

Source: EIKON, Emirates NBD Research

Source: EIKON, Emirates NBD Research

Edward Bell

Edward Bell