Recent Search

Popular Searches

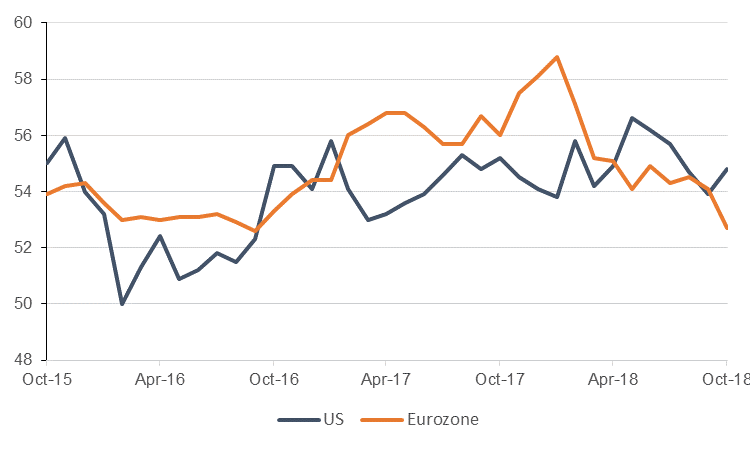

The composite PMI reading for the Eurozone disappointed yesterday, coming in at 52.7, missing expectations of 53.9 and lower than the September reading of 54.1. This signals a slow start to the fourth quarter ahead of the ECB’s meeting later today. Both the services and manufacturing indices posted weaker readings than expected, with manufacturing hitting a multi-year low at 52.1, and new export orders dropping into contractionary territory at 48.9. Nevertheless, the ECB is expected to stick to its plan of ending asset purchases by year-end and raising rates in H2 2019 at its meeting later today, though given rising headwinds there may be a more cautious tone struck.

Also released were PMI results from the US, which exceeded expectations. Manufacturing rose from 55.6 in September to 55.9, beating consensus expectations of 55.3, while services came in at 54.7, beating September’s 53.5 and consensus of 54.0. The composite index rose from 53.9 to 54.8. This is supportive of another strong quarter for the year-end, making a fourth rate hike of the year ever more certain. That said, new home sales data disappointed, slipping from 629k in August to 553k last month, far short of expectations of 625k. This was near a two-year low for the measure and likely reflected the impact that rising interest rates have on homeowners. Trade wars are also on US firms’ minds as the US Federal Reserve’s ‘beige book’ was released last night, illustrating growing concern among US businesses over tariffs. The word and its derivations was mentioned 51 times, having been mentioned only 20 times in the two decades prior to the Trump presidency.

Staying in North America, the Bank of Canada hiked its overnight lending rate by 25bps yesterday, to 1.75%. This was widely anticipated and was the fifth hike since the bank began its monetary tightening cycle in 2017. In its communique the bank talked about bringing rates to neutral levels – a level it estimates is between 2.5% and 3.5% – raising the possibility of more rapid tightening hereon in.

Source: Bloomberg, Emirates NBD Research

Treasuries closed sharply higher amid a rout in risk assets. Yields on the 2y UST, 5y UST and 10y UST closed at 2.83% (-4 bps), 2.93% (-7 bps) and 3.10% (-6 bps).

Regional bonds remained in a tight range. The YTW on the Bloomberg Barclays GCC Credit and High Yield index remained flat at 4.63% while credit spreads widened 5bps to 170bps. It does appear that correction oil prices is starting to weigh on regional credit.

Fixed assigned Dubai Investment Park Development Co a rating of BB+ with stable outlook. Elsewhere, Tabreed raised USD 500mn in a 7-year sukuk which was priced at 5.5%.

CAD was Wednesday’s outperformer in the aftermath of the Bank of Canada’s decision to raise interest rates (see macro). Over the course of the day, USDCAD fell 0.21% to close at 1.3057. A further 0.28% decline this morning has taken the price to 1.3021 with the price likely to test the 50-day moving average (1.3011) today, a level which it failed to sustain a break of, post BOC. Should we see a daily close below this level, it may catalyse a move towards 1.2950, the 100-week moving average, followed by 1.29 not far from the 200-day moving average (1.2914) and our Q4 2018 forecast.

On the other end of the spectrum, NZD is this morning’s underperformer and has softened against the other major currencies after a report from Statistics New Zealand showed that the trade deficit widened to NZD 1559.9Mn in September from a NZD 1470Mn deficit the previous month. As we go to print, NZDUSD is trading 0.10% lower at 0.65229 and remains in the daily downtrend that has been in effect since April 2018. While the price remains below 0.6587, this downtrend will remain intact.

Developed market equities closed sharply lower across as investor sentiment remained weak and corporate earnings mixed. The S&P 500 index dropped -3.1% while the Euro Stoxx 600 index declined -0.2%.

Most regional equity markets closed lower with volumes below 1-month averages. It appears that there was a bout of profit-taking after marginal recent gains. IQCD dropped -2.1% after reporting Q3 2018 net profit of QAR 1.29bn.

Brent futures closed at USD 76.17/b on Wednesday, the lowest level in two months. Risk-off sentiment, a rise in US inventories and pledges by Saudi Arabia to ensure supply have all contributed to the fall in recent days.

Daniel Richards

Daniel Richards