Recent Search

Popular Searches

The outlook for crude oil production in the Middle East and North Africa over the next months will largely be set by US sanctions policy on Iran. US sanctions on trading in Iranian crude will be enforced in full from May, tightening markets in the short term. A production response from other OPEC producers had long been our forecast and is likely to hit markets in the next few months.

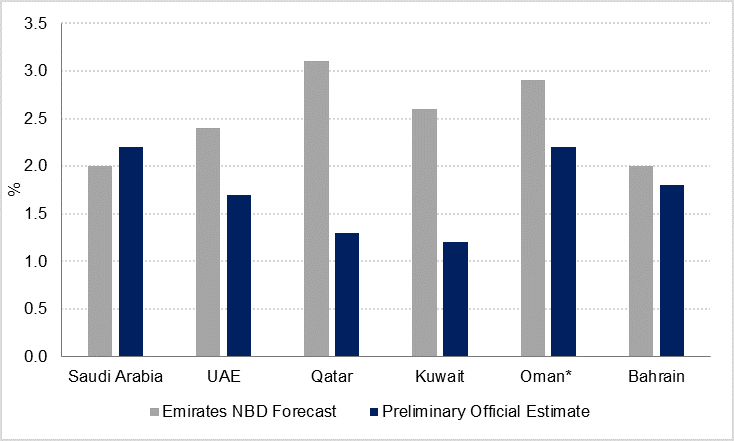

Official GDP growth estimates for the GCC were mostly lower than forecast in 2018. In the UAE, Kuwait and Oman, the weakness (relative to our expectations) was evident in the non-oil sectors, while in Qatar it was hydrocarbons growth that disappointed last year. While the prospect of higher oil production from the major GCC exporters in the coming months is supportive of overall GDP growth in 2019, a recovery in non-oil sector growth will remain reliant on government spending and investment.

We have revised our 2019 growth forecasts for Kuwait, Oman, Bahrain and Qatar down as new estimates for 2018 GDP have become available. We retain our 2.0% growth forecast for Saudi Arabia this year. In the UAE, we await the full release of 2018 GDP statistics before publishing new growth forecasts for 2019 and 2020.

The wider North African region has seen significant unrest in recent months, with renewed hostilies in divided Libya and regime change in Algeria and Sudan following popular protests. It is as yet unclear what forms of government and economic models will emerge in the wake of these changes.

In the rest of the ex-GCC MENA countries the outlook is more positive, as governments implement reforms following periods of stagnation in states such as Lebanon and Iraq.

Source: Haver Analytics, Emirates NBD Research

Source: Haver Analytics, Emirates NBD Research

Click here to download the full report.

Daniel Richards

Daniel Richards