Recent Search

Popular Searches

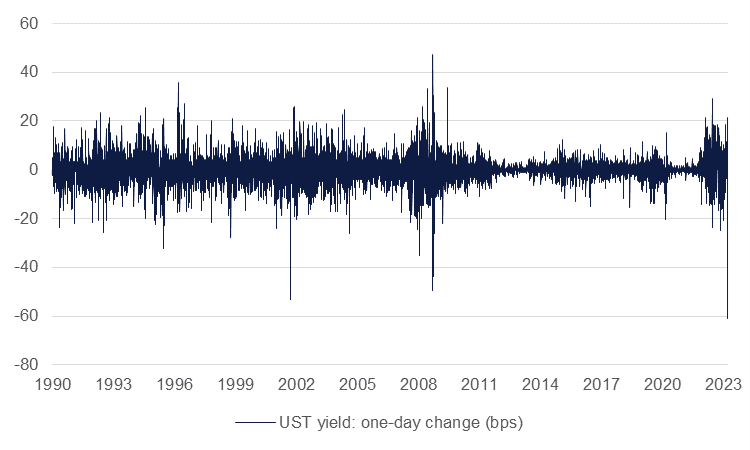

The moves in US Treasury markets have been at historic levels in the wake of the collapse of Silicon Valley Bank, a large tech-focused bank in the US. Yields on the 2yr UST slumped by 65bps from the close on March 10 to their bottom on March 13, moving below 4% for the first time September last year. The drop in UST 2yr yields was the largest in decades, outweighing moves during the Covid-19 pandemic and the height of the global financial crisis in 2008-09.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

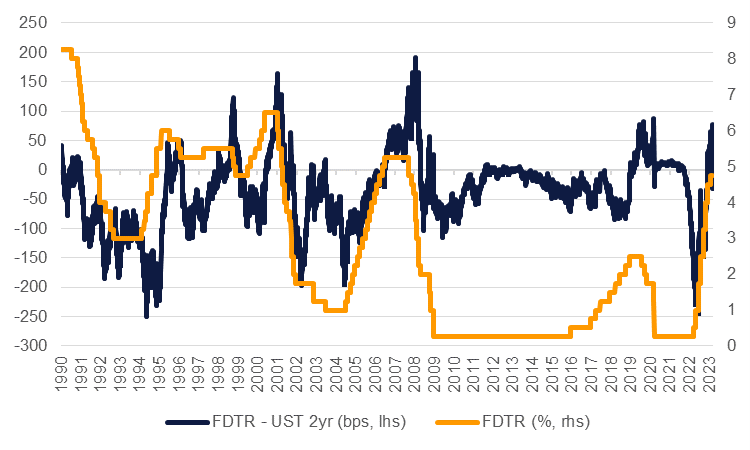

Yields on the 2yr are nearly 60bps below the upper bound of the Fed Funds target rate and the rapid adjustment in UST and market yields suggests that markets think that the Fed hiking cycle will come to a close much sooner than had been expected. Market pricing for the terminal rate is now for 4.8% in May, suggesting just one more 25bps hike before cuts begin from the June meeting onward with rates now priced at barely above 4% by the end of the year. Just one week ago markets had pitched the terminal rate at more than 5.6% as they responded to hawkish commentary from Fed chair Jerome Powell.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

Markets will remain extremely febrile as anxiety widens over the stability of banks in the US with high exposure to certain sectors, tech in particular. But the Fed still has a job to do in preserving price stability and the release of the February CPI print later today will be key for the near-term trajectory for rates, market yields and currencies. Market expectation is still for headline CPI to slow to 6% y/y from 6.4% previously which may give the market some comfort that the Fed won’t need to make use of a large 50bps hike at their FOMC meeting on March 22. Even a 25bps hike is being discounted by markets given the unfolding financial uncertainty in the US.

An on-target inflation print will probably allow the Fed to hike by 25bps even amid the current noise in financial markets. A 50bps hike, as implied by Chair Powell in his testimony to Congress last week, looks out of the question. But market stability in the coming days may also qualify for consideration under the Fed’s “totality of data” and should market conditions worsen from here the Fed may choose instead to pause its tightening cycle.

Edward Bell

Edward Bell