Recent Search

Popular Searches

Markets will enter a slow period with US Thanksgiving holidays on Thursday dampening activity from Wednesday all the way through to the end of the week. An earthquake in northern Japan has brought back some memories of the bigger Fukushima earthquake five years ago, and has given rise to some Tsunami warnings, but the damage is not thought to that extensive this time even though aftershocks could continue for a few more days.

Overall the mood in markets remains relatively optimistic about the US transition even though it happening quite slowly, and today will see some economic data including existing home sales ahead of durable goods orders data that are released tomorrow. Comments from Fed Vice Chair Stanley Fischer yesterday appeared to support the likelihood of a December rate rise, noting that growth and prices are nearing the Fed's mandates. He also added there is reason to believe growth could be a little faster, and indicated that the Fed will be taking fiscal policy and infrastructure investment into account when setting policy.

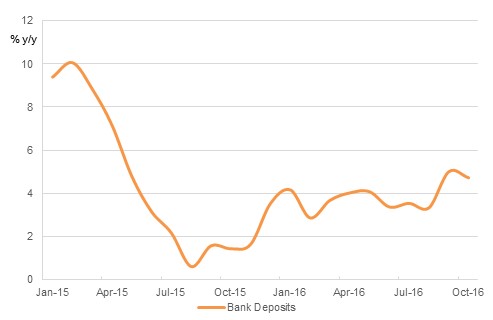

Bank deposits in the UAE fell by 0.4% m/m in October, mainly on the back of lower government deposits (-5.3% m/m). GRE deposits were up 1.2% m/m in October while private sector bank deposits were marginally lower (-0.1% m/m). On an annual basis however, bank deposits were up 4.7% in October. Gross lending increased 0.3% m/m (6.0% y/y), with private sector borrowing up 0.2% m/m and 6.0% y/y. As a result, the gross loan/ deposit ratio rose to 104.5% last month from 103.8% in September. Net loans/ deposits rose to 97.3% up from 96.8% in September. SAMA has appointed Thomson Reuters to administrate and calculate the benchmark SAIBOR rate, effective 20 November. The statement says the move will “allow for further transparency and reliability” in the calculation.

Source: Emirates NBD Research

Source: Emirates NBD Research

|

| Time | Cons |

| Time | Cons |

| EZ Consumer Confidence | 19:00 | -7.8 | US Existing Home Sales | 19:00 | 5.44m |

Market exuberance paused somewhat in a week devoid of any material catalyst and laden with upcoming thanksgiving holiday lethargy in the US. Yields on short term UST remained entrenched at higher level with 2 yr closing at 1.07% (unchanged) after Fed vice chair Stanley Fisher reaffirmed the rate hike rhetoric, however, longer dated UST yields pared down somewhat with 10yr and 30yr closing at 2.32% (-4bps) and 2.99% (-4bps) respectively.

Credit spreads across the globe received a boost from increasing optimism about rising oil prices. CDS levels on US IG and Euro Main both closed at bp tighter at 76bps and 81bps respectively while those on the GCC sovereigns such as SA and Qatar also narrowed to 130bps (-5bps) and 91bps (-3bps) respectively.

GCC cash corporate bonds benefited not only from a 4% increase in oil prices but also from stalling long term UST yields and credit rating affirmation of SABIC (A-/stable), Dolphin Energy (A+/stable) and IPIC (AA/stable). BUAEUL index closed up higher with YTW falling a bp to 3.10% and credit spreads also tightening a bp to 156bps. Bloomberg Barclays GCC bond index that includes bonds from the other five sovereigns in the region also saw credit spreads tighten by 4bps to 145bps.

Primary market has Etihad Airways on the road, however the deal is being placed privately. EA is rated A by Fitch and initial price guidance of circa 200bps over 5yr MS appear fair with some scope for further tightening.

Developed market equities started the week on a positive note amid sharp rise in oil prices. The S&P 500 index rallied +0.8% to touch new all-time highs as investors continue to place their trust in Donald Trump’s proposed economic policies. The Euro Stoxx 600 index added +0.3%.

Asian equities are trading higher this morning tracking strong close to developed markets overnight. The MSCI Asia Pacific index was trading +0.5% at the time of this writing.

The Tadawul (-1.1%) was a notable exception in what was largely a subdued day of trading in regional equity markets. The Tadawul closed lower for a third consecutive trading session indicating that investors are locking in gains after a nearly 20% rally since mid-October 2016. Healthcare stocks continue to underperform with Dallah losing -2.4%.

Elsehwere, the EGX 30 index continued its positive run with the index rallying +2.4% amid a fresh leg of weakness in the EGP. Real estate stocks continue to outperform the market with TMGH adding +4.2%.

Currency moves have been relatively muted after the strong USD gains of the last few days with a tone of consolidation starting to develop ahead of US holidays towards the end of the week. The JPY has strengthened a little in response to the 7.3 earthquake in Fukushima which has occurred overnight. GBP also leapt yesterday in thin trading as PM May appeared to suggest in a speech to British industry representatives that she may be open to a transitional trade deal with the EU, calming some fears that the UK might be headed towards a ‘hard Brexit’.

Oil markets were up sharply to start the week as optimism over the potential for an OPEC deal spreads. WTI and Brent futures closed up either side of 4% and broke above the longer term moving averages for the first time since the start of November. Brent is now within sight of USD 50/b, which it will easily break above if the odds of an OPEC deal shorten over the next week. We expect something constructive out of the OPEC meeting, with the lowest cost option being an announcement similar to what we saw in Algiers. But proof of any reduction in volumes will only be apparent in the first few months of 2017.