Recent Search

Popular Searches

Indian financial assets are at crossroads as steps taken by the government to revive animal spirits are taking longer than anticipated and the slowdown in the domestic economy becomes more entrenched. The limited fiscal and monetary space available to policymakers coupled with increasing global risks has raised the odds of a rather volatile first half of 2020 for Indian markets.

The overarching aim of the budget presented by the government appears to be to revive the private investment cycle. Further, the government is seeking to complement that by continuing to keep public spending robust and by making India an attractive destination for foreign capital. The strategy appears to be a continuum of the steps announced before the budget which included slashing corporate tax rates. The government, additionally, has taken some steps to rationalize income taxes in its bid to revive consumer demand. However, in our opinion, they fall well short of expectations and are expected to have limited impact.

The primary vehicle used by the government in its bid to revive the private investment cycle has been to free up capital in the hands of private companies. Following the sharp rationalization in corporate tax rates, the government in its budget abolished the dividend distribution tax (DDT) and made the dividend income taxable in the hands of the recipient. The change in tax law also covers Indian subsidiaries’ upstreaming profits to foreign holding companies. The government estimates that this will result in a revenue loss of INR 250bn.

Together with cuts in corporate tax rates which is projected to lose government revenues worth INR 1.45tn, the total cash freed up for Indian corporates stand at INR 1.7tn. According to preliminary data available, nearly half of companies in the Nifty 50 index had switched to lower corporate tax rates for the quarter ended September 2019.

The working behind this method of providing stimulus to corporates seems to be that they will deploy extra cash available in fresh capital expenditure which in turn will create new job opportunities and eventually stimulate more durable consumer demand.

| FY 2019 | FY 2020 (RE) | FY 2021 (BE) | |

|---|---|---|---|

| Gross Tax Revenue | 15.5 | 18.5 | 20.2 |

| Non Tax Revenue | 2.4 | 3.5 | 3.9 |

| Disinvestment | 0.9 | 0.7 | 2.1 |

| Revenue Expenditure | 20.1 | 23.5 | 26.5 |

| Capital Expenditure | 3.1 | 3.5 | 4.1 |

| Revenue Deficit | 4.5 | 5.0 | 6.1 |

| Gross Fiscal Deficit | 6.49 | 7.67 | 7.96 |

| Fiscal Deficit % of GDP | 3.4 | 3.8 | 3.5 |

Source: Union Budget Documents

As part of two-pronged approach to drive investments into the country, the government appears to have embarked on an irreversible course of attracting foreign capital. In addition to measures announced earlier, the government in the budget made proposals to fully open certain categories of government securities to non-resident investors and increased the limit of foreign portfolio investments in corporate bonds from 9% to 15%. Both these measures appear to be aimed at signaling a readiness to join the global bond indices. Interestingly this comes at a time when foreign investors have reduced local debt holdings to a multi-month low.

Source: Bloomberg

Source: Bloomberg

Further, the government said it will grant 100% tax exemption on interest, dividend and capital gains on investments made in infrastructure by sovereign wealth funds before 31 March 2024. The same would be subject to a three-year lock-in period.

For the better part of the last 12 months, the government has been doing the heavy lifting in terms of spending and the budget for FY 2021 follows the same principle. Importantly, the quality of spending continues to remain high with capital expenditure expected to increase 17% to INR 4.1tn while revenue expenditure is expected to grow 12% to INR 26.3tn. The ratio of capital expenditure to GDP is projected to grow from 1.6% in FY 2019 to 1.8% in FY 2021.

We do note, however, that much of the proposed increase in expenditure is reliant on robust revenue collections and that in the past the government has resorted to expenditure cuts. For example, the total expenditure in FY 2020 is forecast to decline by 3.2% compared to initial budget estimates.

The government for the first time in the recent past used the escape clause under the FRBM Act (Fiscal Responsibility and Budget Management Act) to breach its fiscal deficit target of 3.3% for FY 2020. The government now projects FY 2020 fiscal deficit at 3.8% and FY 2021 fiscal deficit at 3.5%. This on face value indicates a return to fiscal consolidation.

However, it is worth noting that the reduction in fiscal deficit is primarily dependent on a very aggressive non-tax revenue target of INR 3.9tn which includes an asset sale program of INR 2.1tn. The aim appears ambitious and will largely depend on the government’s ability to carry out divestments of key assets including Air India, Life Insurance Corporate (LIC) and BPCL. Beyond the divestment targets, the projected increase in tax collections looks modest and should be achievable.

Another way of looking at the composition of revenue and resultant fiscal deficit is that the government is actually providing a stimulus as fiscal deficit excluding asset sales would increase from 4.1% of GDP in FY 2020 to 4.5% in FY 2021.

After having reduced interest rates by 135 bps over the last twelve months, the Reserve Bank of India (RBI) kept rates on hold for a second consecutive meeting. The current repo rate of 5.15% is the lowest level since 2010. Notwithstanding the pause in monetary policy easing, the central bank retains an accommodative stance. Having said that, the priority is now balanced between spurring growth and maintaining price stability. It should also be noted that interest rate cut transmission to the real economy generally takes 3-6 months which in effect indicates that the full impact of easy monetary policy may not have yet worked its way through the economy. Indeed over the last 12 months, the 1-year median marginal cost of funds-based lending rate (MCLR) has declined by 55 bps so far.

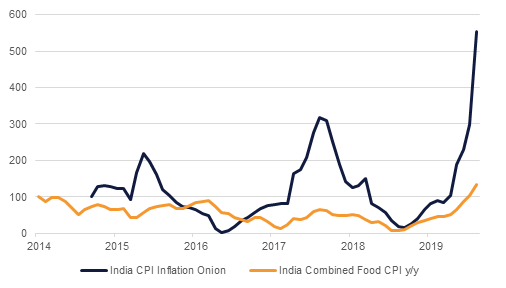

The pause in the interest rate cuts by the RBI can also partly be attributed to domestic pressures. The CPI for December 2019 came in at 7.35% y/y. This was the first reading above the central bank’s upper band target of 6% since July 2016. The spike in inflationary pressures over the recent months has largely been on account of higher food prices and lower base effects. Even within the food basket, the driving force has been onion prices. Encouragingly for the central bank, core inflation remains benign at 3.4% y/y. Having said that, the surplus monsoon rains and winter harvesting data suggest that food price pressures should ease from here on, relieving pressure on headline inflation.

Source: Bloomberg

Source: Bloomberg

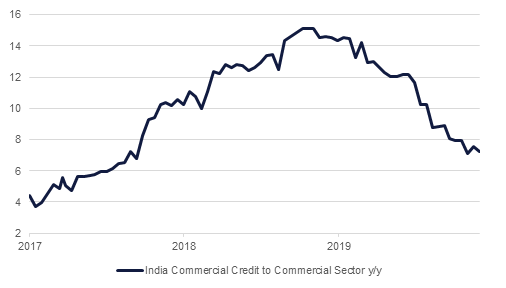

Looking ahead, we expect the RBI to remain on prolonged pause. The counter cyclical fiscal measures announced by the government in the budget and some signs of economic recovery should provide the central bank with enough grounds to stay put on monetary policy. It is also likely that the RBI will, for the time being, take high inflation in their stride and retain an accommodative bias. With little room for interest rate cuts, we expect the RBI to continue with quasi operation twist in its attempt to keep short-term bonds yields on a tight leash. The RBI so far has bought INR 400bn of long-term bonds and sold INR 282.8bn of short-term bonds. The RBI can take more unconventional measures like its decision at last month to exempt banks from setting aside mandated cash reserve when giving new loans to automobiles, residential housing and loans to SME and MSME. This should provide an impetus to a sluggish credit growth.

Source: Bloomberg

Source: Bloomberg

Following the Q2 FY 2020 GDP reading of 4.5%, the lowest quarterly reading since mid-2013, high frequency indicators have shown signs of recovery. Before we dwell on that, it must be highlighted that all agencies including the RBI and IMF have lowered India’s full year FY 2020 growth to sub-6%. The CSO estimates India’s FY 2020 GDP to come in at 5%. For FY 2021, the government’s economic survey projects GDP growth between 6% and 6.5%.

The latest PMI data for January 2020 has come in at multi-year highs with Markit manufacturing PMI reading of 55.3 and Markit Services PMI at 55.5. Importantly, the PMI data indicates expansion across its various sub-indices of output, new orders, and employment. The industrial production and eight infrastructure industries data also surprised positively with readings of 1.8% (versus -3.8% in the previous month) and 1.3% (versus the previous month’s reading of -1.5%) respectively.

The external sector continues to remain a source of comfort. India’s merchandise trade deficit in December 2019 moderated to USD 11.3bn on the back of higher non-oil exports and weak imports. On an m/m basis, core exports grew 7.2% even as annualized exports contracted by 1.8%. The current account deficit is expected to moderate to 1.0% of GDP in FY 2020 from 2.1% in FY 2019.

It does appear that simultaneous measures taken by the RBI and government over the past few months are finally starting to bear fruit. However, we believe that it is too early to suggest that growth has bottomed out. Further, global risks continue to remain elevated and that in turn could very well puncture the visible early cycle growth.

Notwithstanding the sharp slowdown in economic activity, Indian equity markets have tracked global indices and in fact outperformed their emerging markets peers. The Nifty index has dropped -1.7% 1m but gained +1.4% 3m. Relative to emerging markets, return from Indian equities is better. The total return from MSCI India (USD index) in January 2020 was -0.8% compared to -4.7% in the same month from the MSCI Emerging Markets USD index. Volatility has increased sharply with the INVIXN index jumping +23.0% ytd.

The interesting feature in gains over the past three months has been the outperformance of midcap stocks. The Nifty 50 midcap index has rallied +6.6% 3m. This is in sharp contrast to the performance in 2019 where the Nifty 50 midcap index dropped -4.7% compared to gains of +12.0% in the Nifty 50 index.

The sectoral performance over the last three months reflects the concerns in the wider economy. Telecom, Financial and Technology sectors stocks are the only ones which have delivered positive returns while other sectors have underperformed. Consumer goods sector stocks (-2.6% 3m) stand out amid continued concerns over slowing economic growth. Oil & Gas sector stocks are another one which has underperformed reflecting the sharp fall in oil prices. Brent prices have dropped -12.1% 3m.

The fund flow from foreign institutional investors (FIIs) continued to remain robust. Foreign investors bought stocks worth USD 2bn in January 2020, sharply higher relative to inflows of USD 862mn in December 2019. Domestic institutional investors (DIIs) turned net buyers for the first time in three months. They bought stocks worth USD 316mn in January 2020. Within DIIs, mutual funds were net equity buyers while insurance funds were net sellers.

In the first month of 2020, yields on 10y government bonds rose +5bps to 6.60% as worries over the government’s financing program amid weak growth dynamics outweighed moves in global benchmarks. In contrast, the YTW on Bloomberg Barclays EM Local Currency Government index dropped 16 bps to 3.56% and on 10y US Treasuries dropped -32bps to 1.50%. The move in global benchmarks was primarily on account of concerns from the outbreak of coronavirus. With the government signaling fiscal consolidation and keeping borrowing plans benign, we expect pressure on yields to ease.

January marked the third consecutive month when FIIs were net sellers in the debt market. Following an outflow of USD 756mn in December 2019, FIIs sold bonds worth USD 1.6bn in January 2020.

On the corporate debt side, it is worth highlighting that the credit scores of Indian borrowers are worsening. According to data from India Ratings & Research Pvt Ltd, the credit scores of 188 Indian borrowers were lowered in the first nine months of FY 2020, compared with 103 upgrades. It is the worst ratio since FY 2012. In terms of value about INR 1.53tn of debt was downgraded, three times as much as the value upgraded.

The INR has started 2020 on a strong footing. So far, it is among the best performing emerging market currencies with gains of +0.2% compared to a decline of -1.9% in the JP Morgan EM FX index. The outperformance can be attributed to reduced pressure from oil prices, an expectation of an economic recovery and sustained inflows into equities from foreign institutional investors. Interestingly, according to Bloomberg, INR is the cheapest currency in the world with more than 70% undervalued to the USD (IMF metrics).

With the domestic economy exhibiting green shoots and the government continuing to take steps to attract foreign capital, we expect the INR to remain rather range bound. However, there are enough risks on the horizon which could act as dampeners. These include sustained disruption in emerging markets’ economic activity due to coronavirus and fresh escalation in geopolitical tensions among others. However, from a medium term perspective, we see risks as fairly balanced. Accordingly, we forecast INR to end Q1 2020 at 71.0 levels and appreciate marginally over the year to 69.0 by the end of 2020. These projections also take into account our broad view that the USD will weaken slightly in 2020 as domestic US politics takes center stage and a dovish stance from the US Federal Reserve continues.

Aditya Pugalia

Aditya Pugalia