Recent Search

Popular Searches

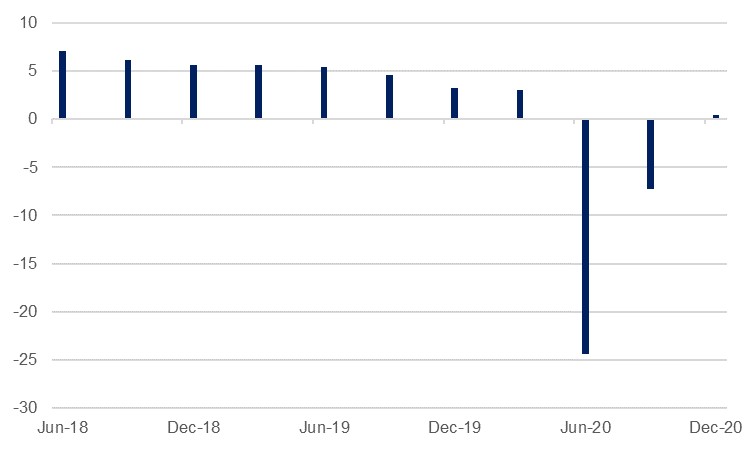

The government of India has pledged a fiscal stimulus package of USD 265bn to help the economy weather the fallout from the coronavirus outbreak. While greater details of the package will be unveiled over the next few days, the quantum amounted to nearly 10% of India’s GDP making it one of the largest announced globally so far. The need for such a package is evident from the recent economic data. Industrial production data for the month of March 2020, released yesterday, fell by a record 16.7% y/y, steeper than consensus expectations of a -8.0% drop. Further, the CPI for the month of April was not released as data collection was hampered due to nationwide lockdown while the CPI reading for March 2020 was revised slightly lower to 5.84%.

US inflation came in broadly in line with expectations in April, at -0.8% m/m (compared to -0.4% in March) and 0.3% y/y (down from 1.5% the previous month). Of particular note was the fact that core inflation’s -0.4% m/m was the strongest downward move in series data back to 1957. This will be concerning to policy makers who will be wary of an emerging deflationary environment exacerbating the pandemic recession. Fed chair Jerome Powell is due to speak on economic issues later today, where market observers will be looking for any indication that the central bank might yield to mounting pressure – including from US President Donald Trump’s latest tweets – to take rates negative.

IMF managing director Kristalina Georgieva has cautioned that the Fund’s growth forecasts are likely to be revised down. The IMF published its last major growth projections in mid-April when it predicted a -3.0% contration in GDP, but Georgieva acknowledged that the scope of the pandemic meant that this was likely not sufficiently bearish, with a host of major economies faring far worse than previously anticipated.

Within the region, different economies are at differing stages with regards economic shutdowns. The UAE is looking to tentatively introduce additional easing after Ramadan, further to that seen since the start of the month, and is drawing up a post-pandemic long-term stimulus plan which will focus on the digital economy. In Lebanon, meanwhile, which was already struggling with an economic and financial crisis which has seen it go to the IMF for assistance, the country has ordered a renewed shutdown after some gentle easing previously has led to a resurgence in cases.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

Treasuries closed higher on the back of weakness in US equities and as 10y auction saw very strong demand. The curve bull flattened with yields on the 2y UST and 10y UST ending the day at 0.16% (-1 bp) and 0.66% (-4 bps) respectively.

Regional bonds continued their positive run unabated. The YTW on Bloomberg Barclays GCC Credit and High Yield index dropped -3bps to 3.72% while credit spreads remained flat at 308 bps.

Mubadala raised USD 4bn from a three-tranche bond offering. The 6y tranche (USD 1bn) was priced at MS+210 bps, the 10y tranche (USD 1bn) at MS+235 and the 30y (USD 2bn) tranche was priced to yield 3.95%.

The dollar reversed a lot of its gains on Tuesday following Monday's sharp advance, briefly dropping to 99.663 but finding support at this area to now trade at 99.990. U.S. President Donald Trump supported the idea of negative rates in the country but Federal Reserve officials have dismissed the notion, creating uncertainty ahead of the Fed's announcement on Wednesday. The JPY made some modest gains after Monday's decline to reach 107.20.

Market sentiment seems to have stabilized within Europe ever so slightly, with the euro in bullish mood for the day. The currency met resistance at 1.0885, but still maintained an increase over 0.35% from the closing price at 1.0845. Sterling meanwhile declined by over -0.60% amidst uncertainty surrounding U.K. PM Boris Johnson's new lockdown instructions, to reach 1.2260. The AUD was largely unfazed for the day, trading at at 0.6460 whlst the NZD declined by over 1.15% to 0.6010.

Developed market equities traded mixed as several Fed officials presented a dire outlook on the economy. The Euro Stoxx 600 index added +0.3% while the S&P 500 index lost -2.0%.

Regional equities rebounded from previous session losses. The DFM index and the Tadawul added +0.5% and +1.2% respectively. Saudi Aramco reported Q1 2020 earnings of SAR 62.5bn (-25% y/y) and announced the quarterly dividend payout of USD 18.75bn to remain on track for full year dividend payout of USD 75bn.

Egyptian stocks rallied sharply after the IMF approved an emergency pandemic aid of USD 2.77bn. The EGX 30 index added +2.8%.

Oil prices gained overnight as more countries joined with Saudi Arabia to deepen their production cuts for June. Brent added a little more than 1% to settle just shy of USD 30/b while WTI was up almost 6.8% at USD 25.78/b. Both are nudging slightly lower in trading this morning.

The EIA cut back its projection for US supply in 2020 by an additional 70k b/d to 11.69m b/d and by 130k b/d for 2021, meaning annual average production of 10.9m b/d. In January the EIA expected oil production of more than 13m b/d in 2020 but the coronavirus pandemic has ravaged oil markets and caused a dramatic collapse in drilling activity.

Private sector stockpile data showed a rise of 7.6m bbl in the US last week. EIA data is expected later today which is likely to confirm a persistent trend of inventory builds.

Daniel Richards

Daniel Richards