Global trade threats have abated slightly and the geopolitical tone has improved a little as well. However, these issues have not gone away and could still be a headwind to markets as well as to growth. Some hesitancy is observable on the part of global policymakers, and in the GCC growth risks appear to be to the downside on the back of developments in both the oil and non-oil sectors.

- Global macro: Although concerns about trade have abated a little, these risks along with geopolitical ones still remain as a potential headwind to growth. Indeed some policymakers, in Europe for example, appear to be a little more hesitant about the outlook.

- GCC macro: As we take stock at the end of the first quarter, the economic data has been a little underwhelming in most of the GCC region.

- MENA macro: As May 12 approaches, it is unclear whether or not US President Donald Trump will refuse to renew the waivers on sanctions against Iran and its nuclear programme. The effect of such a move on the Iranian economy would be highly negative, but we see scope for some concessions to be made by both sides as the deadline nears.

- Sector focus: An update on UAE education sector.

- Emerging Markets Focus: India

- Interest rates: Solid economic growth and receeding fears of trade wars pushed the UST yield curve above its February highs, taking most of the DM sovereign yields higher.

- Credit: Driven by rising benchmark UST yields, global corporate bonds generally fell in price during the month, even though credit spreads had a tightening bias on the back of solid economic growth and positive results announcements.

- Currencies: Breaking from seasonal norms, the dollar has appreciated in April for the first time since 2010.

- Equities: It was a month of two halves for global equity markets. While trade war and geopolitical risks dragged equities lower at the start of Q2 2018, a robust start to the earnings season coupled with fading trade concerns helped equities recover some of their losses. Even as all these risks continue to remain on the horizon, we are cautiously optimistic on global equity markets.

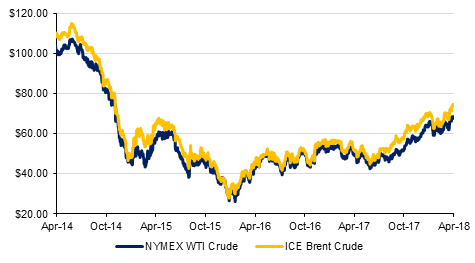

- Commodities: Oil prices are holding at their highest level since the end of 2014. Policy and fundamental factors are helping to support prices in the near term and this month we highlight the upside risks to our forecast. Aluminium prices have moved onto a new higher footing following the imposition of US sanctions on a major Russian producer.

Oil prices back to levels last seen in 2014

Source: Emirates NBD Research, Bloomberg

Source: Emirates NBD Research, Bloomberg

Click here to Download Full article