Recent Search

Popular Searches

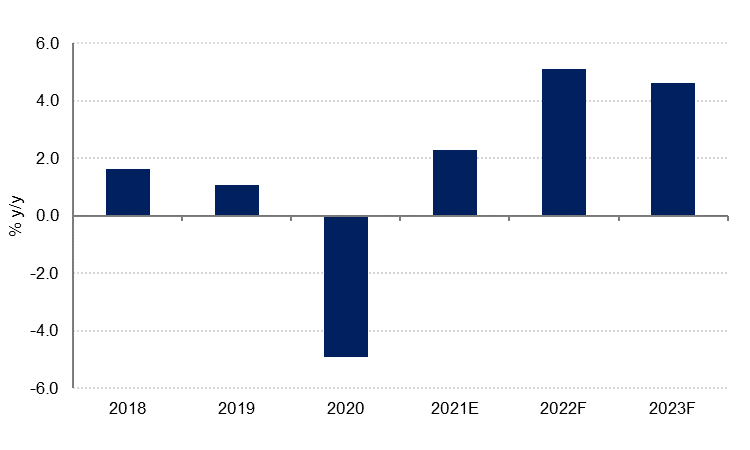

Despite relatively tight fiscal policy, and some external headwinds, we expect the GCC economies to see faster growth in 2022 as they continue to build on the progress made last year. Overall, we forecast GDP growth in the GCC will accelerate to 5.1% on a nominal GDP-weighted basis in 2022, with the oil and gas sector contributing meaningfully to this faster growth.

The recovery in the GCC economies gained momentum in the second half of 2021 as travel restrictions eased, tourism rebounded and domestic demand strengthened. Regional PMI surveys pointed to an acceleration in non-oil sector growth in the UAE, Saudi Arabia and Qatar, while the OPEC+ agreement to gradually increase oil production from July contributed to a recovery in the oil and gas sectors as well.

Overall, we estimate GCC economies grew 2.3% in 2021 (on a nominal GDP weighted basis) following a contraction of -4.9% in 2020. The economic recovery in the region last year was more gradual than the sharp rebound in some of the major developed economies, including the United States, partly due to the size of the hydrocarbons sector and partly because direct fiscal stimulus during the Covid-19 pandemic was smaller relative to many other countries.

* Nominal GDP weighted average

* Nominal GDP weighted average

Source: Haver Analytics, Emirates NBD Research

Last year GCC governments prioritized reduction of budget deficits, which had widened sharply in 2020, rather than accelerating GDP growth through increased spending. The recovery in oil prices last year helped to narrow deficits, but governments also remained committed to their tighter spending plans and other fiscal reforms that had been introduced in 2020. GCC governments have focused on accelerating the pace of structural reforms to attract private and foreign investment and thereby support economic growth over the medium term.

We expect this approach to continue in 2022. Saudi Arabia, the region’s largest economy, has pencilled in a 6% decline in spending in the 2022 budget even as revenue projections were increased. With Brent oil forecast to average just under USD 70/b in 2022 and GCC oil production expected to rise, we expect Saudi Arabia, the UAE and Qatar to post budget surpluses this year, while Oman and Bahrain are likely to see their budget deficits narrow further.

Investment by government related entities and sovereign wealth funds will remain a source of growth in the GCC, even as direct budget spending may be contained. And while global growth will slow this year relative to 2021, it will likely remain supportive for the region at 4.9%.

While the outlook for 2022 remains broadly constructive, there is still a high degree of uncertainty especially with regards to the evolution of the coronavirus pandemic. The recently identified Omicron variant appears to be much more easily transmitted and has led to a surge in Covid-19 cases globally that far exceeds previous peaks. This has led to renewed travel restrictions and lockdowns in some countries, mainly in Europe and parts of Asia, which will likely weigh on economic growth in the near term.

In the GCC, vaccination rates are relatively high – in the UAE 99% of the population has received at least one dose of a Covid-19 vaccine - and the population is young. Consequently, we expect the GCC economies to remain open with few restrictions on movement and activity. Even if the current wave of Covid-19 infections weighs on services sectors (particularly tourism and hospitality) in the near term, we expect the impact on the broader economy will be limited.

Another potential risk to the outlook for 2022 relates to the withdrawal of the exceptional stimulus injected into the global economy in 2020, which could likely to lead to heightened volatility in financial markets and provide a further headwind to growth in the GCC in the form of higher borrowing costs and a stronger US dollar in the GCC.

In our view however, the structural reforms implemented over the last couple of years, along with a much stronger fiscal position and recovering domestic demand, will support growth in the GCC in 2022 and beyond. In the UAE, these reforms include the expansion of longer-term residency visas to broader categories of residents and new pathways to citizenship, wide-ranging changes to personal and labour laws, allowing 100% foreign ownership of onshore companies and most recently, the decision to align the UAE’s working week with that of major economies. In Saudi Arabia, significant progress has been made in tackling red tape, implementing wide-ranging social reforms and investing in infrastructure to enable greater private sector investment and participation in the economy.

Khatija Haque

Khatija Haque