Recent Search

Popular Searches

The G20 meeting remains the focus for markets with a relatively tepid start to the week. Senior trade officials from both China and the US held talks overnight to try and restart dialogue which has broken off since the start of May. The US Trade Representative, Robert Lighthizer, and Treasury Secretary, Steve Mnuchin, agreed to keep communication open with their counterpart, Liu He, the Chinese Vice Premier. Donald Trump will apparently be happy with “any outcome” from talks with Xi, his Chinese counterpart, suggesting the chances of getting some kind of agreement are roughly balanced. Trump also attacked the US Federal Reserve again over Twitter, saying the central bank “blew it” by raising rates too fast and removing quantitative easing from the market. Speculation has floated around in markets that Trump may seek to remove or demote Jerome Powell, the Fed chair, in favour of a more compliant leader at the Fed who presumably would cut rates.

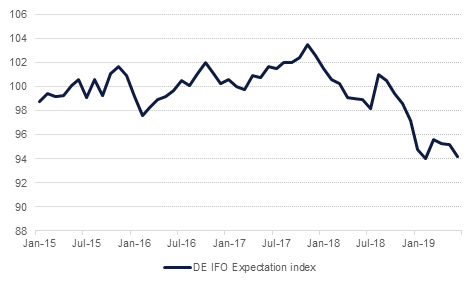

Germany’s economy reported another set of disappointing data as the IFO survey of business climate dipped to 97.4 for June, from 97.9 previously. The forward looking component weakened to 94.2 as manufacturing remains lackluster and global trade tensions are elevated. The current conditions component moved up slightly to 100.8 from 100.7 a month earlier. The IFO data reinforces the view from last week’s PMI data that showed Germany as a relative underperformer among Eurozone economies and compounding the call on the ECB to provide further stimulus to support regional growth.

The central bank of the UAE has estimated Q1 2019 GDP growth at 2.2% in the UAE, with non-oil sector growth estimated at 1.6% and oil sector growth at 4.2%. We have revised our GDP growth forecast for 2019 down to 2.0% from 3.1% previously, in line with the central bank’s forecast for the full year.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

Yields on US Treasuries sagged to begin the week, falling nearly 5bps on 10yr USTs. A Fed on hold and eleveated geopolitical risk linked to China-US trade talks and tensions in the Gulf is supporting a move to risk-off assets like US Treasuries.

The dollar pushed lower to start the week as markets maintain expectations that the Fed will cut rates later this year and risk-off assets come into play. Sterling ended the day roughly flat while the Euro managed to edge higher. News of an opposition candidate winning the mayoralty of Istanbul helped Turkish lira strengthen to 5.808.

Markets generally were weaker to start the trading week although movements were relatively limited. Until more clarity over the outcome of US-China trade talks hit markets we would expect investors to keep to the sidelines. The S&P 500 ended the day down 0.17% while the Dax in Germany saw larger declines. Regional markets were mixed with the Abu Dhabi exchange up 0.5%, the DFM flat and the Tadawul losing 1.6%.

Oil markets are falling again this morning as focus shifts to the G20 meeting and prospects for trade and global oil demand. Brent futures are down nearly 0.8%, extending yesterday’s decline while WTI is getting close to a 1% drop, erasing yesterday’s gains. The US imposed more sanctions on Iran overnight, directly targeting the country’s leadership but there has been no significant change to the odds of a clash in the Gulf region.

Russia’s energy minister said that cooperation on oil markets was “more important than ever” ahead of talks with OPEC next that aim to extend the current level of production cuts. Russia has been relatively non-committal compared with other producers in OPEC on whether the market needed cuts to be extended in H2 2019.

Edward Bell

Edward Bell