Recent Search

Popular Searches

The European Central Bank is picking up the hawkish baton from the Federal Reserve and looks set to continue with large hikes at upcoming meetings. A slew of governing council speakers in recent days have talked up the need to keep hiking by 50bps, on pace with the increase in policy rates the ECB undertook in December. Klaas Knot, head of the Dutch central bank, said that 50bps would be the “pace for a multiple number of meetings” and that the inflation outlook for the Eurozone was still “far away from” when they could decelerate to 25bps hikes. Knot’s counterpart from Finland, Olli Rehn, also noted that there were “grounds for significant increases” while the head of the French central bank, Francois Villeroy de Galhau, also supported getting rates to a restrictive level and holding them there.

Most critically, Christine Lagarde, president of the ECB, has also described inflation as “way too high” and that rates need to move to a restrictive stance “for long enough to return inflation to 2%.” Earlier this week, Lagarde said that the ECB would “stay the course” and warned that core inflation was still rising even if the Eurozone was benefitting from lower natural gas prices, at least for now. Lagarde had said at the December meeting that another 50bps hike was tacked on for the “next meeting, and possibly the one after that, and possibly thereafter” and market expectation of a 50bps hike at next week’s ECB meeting (February 2nd) is entirely priced in. Markets are also looking for another 50bps in March though are more undecided about the May meeting.

The hawkishness from the ECB is all the more striking compared with the turn from Fed speakers to support a 25bps hike at the next FOMC (also on February 2nd). To be certain, no Fed officials have said they need to move to an accommodative stance on policy but rather that the economy warrants a further downshift in pace to 25bps after the Fed moved to a 50bps hike in December. Christopher Waller, a Fed governor, said he supported a 25bps hike for February, backing up calls from Patrick Harker (Philadelphia, voter), Raphael Bostic (Atlanta, non-voter) and Susan Collins (Boston, non-voter) for a slower pace of hikes.

Currency markets are highlighting the split in tone with EURUSD up nearly 2% since the start of the year at around the 1.09 level while the broad dollar index, admittedly weighted heavily against the Euro, has fallen by about 1.7% this year. Amongst other major peer currencies, sterling has had a strong start to 2023, rising by 2.7% year-to-date to around 1.24, levels not seen since the middle of 2022. The theme of a weaker dollar is playing out across the board of G10 currencies with CAD, AUD and NZD all posting gains at the expense of the greenback. USDJPY has also moved in favour of the yen though the Bank of Japan’s persistence in maintaining a dovish stance is capping gains for the yen.

Optimism is also spreading that any recessions in major economies could end up being avoided this year or may be only mild. This turn in sentiment has been rapid but has been borne out by economic data performing better than expected, even if a slowdown in activity is still visible. The easing gloom is cutting across geographies though the US is a notable outlier. The improving outlook for 2023—with even the hitherto downbeat IMF saying it needed to revise its expectations for the year upwards—is helping to spur on risk sentiment and accelerate the narrative of the US dollar softening against peers.

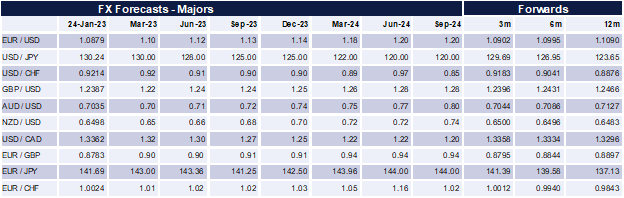

We had expected to see the dollar soften against major currencies this year and we are now bringing that expectation forward. For EURUSD we now have a targe of 1.10 by end of Q1 before gaining to 1.14 by end of the year. In GBPUSD, we have a target of 1.22 by end of Q1, rising to 1.25 by the end of the year. For USDJPY, on the assumption that a change in Bank of Japan leadership brings about more effort to normalize policy, we expect that the pair will fall to 125 by end of the year.

If the current economic optimism dissipates thanks to a resurgence of high energy costs for instance or another exogenous shock, then the dollar would again be a beneficiary of a flight to safety. But for now, it appears that the dollar has peaked.

Emirates NBD Research FX assumptions

Source: Bloomberg, Emirates NBD Research.

Edward Bell

Edward Bell