Recent Search

Popular Searches

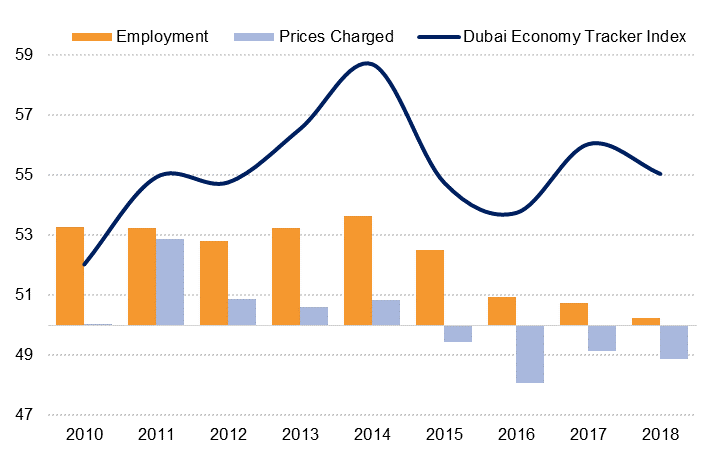

The headline Dubai Economy Tracker Index declined to 53.7 in December on slower output and new order growth. The average DET reading for Q4 was 53.8, the lowest since Q1 2016. Looked at another way, the last time the DET was at a similar level, the average oil price was USD 47/b rather than the USD 68/b average in Q4 2018.

While private sector firms reported solid increases in output in December, and indeed for the year as a whole, this has come on the back of consistent and continued price discounting in a very competitive environment, despite rising input costs. The prices charged index improved to 48.0 in December 2018, from a near-record-low of 45.8 in November but still indicated lower selling prices last month.

The pressure on firms’ margins and efforts to find costs savings is reflected in almost no job growth in Dubai’s private sector last year: the employment index averaged 50.2, the lowest in the 8 year survey history. Firms have also become more adept at managing their pre-production inventory; stocks of purchases in December rose at the slowest pace since early 2016 in December.

Despite the softness in the December survey, firms were still optimistic about their future prospects. 64% of firms surveyed believed that their output would be higher in a year’s time, while just 5.3% of firms expected further weakness. However, the degree of optimism was the weakest since July 2018.

Source: IHS Markit, Emirates NBD Research

Source: IHS Markit, Emirates NBD Research

Overall, the Dubai Economy Tracker index data suggests that Dubai’s economy grew at roughly the same rate in 2018 as in 2017. Preliminary official estimates put GDP growth at 2.8% in 2017 and we have pencilled in the same for 2018. This is slower than we had anticipated at the start of last year. We do expect GDP growth to accelerate in 2019 however, as government spending is likely to rise and as the bulk of Expo 2020 projects near completion.

Khatija Haque

Khatija Haque