Recent Search

Popular Searches

Japan’s Prime Minister Shinzo Abe said he’ll dissolve the lower house of parliament on Sept. 28 for a general election partly to ascertain the support for him and his party after their hard stand on the North Korea issue. Abe added that he’d resign if his ruling coalition failed to get a simple majority. He also announced a 2 trillion yen ($18 billion) economic package, including spending on preschool, higher education and elderly care. This new spend will be funded by revenues from a planned increase in the nation’s consumption tax in October 2019 to 10% from 8% now. Abe’s support is likely to be buoyed by the economy, which has grown for six straight quarters.

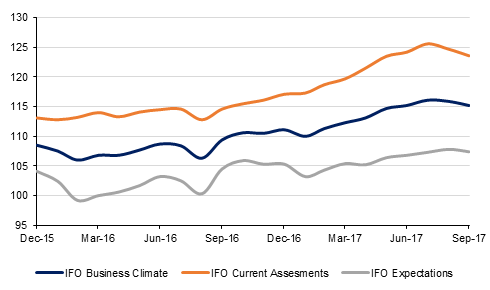

IFO September German Business Confidence Index (BCI) came in at 115.2, slightly weaker than the expectations of 116 and lower than August’s 115.9. Both the current conditions and expectations indices declined. The decline, to some extent, is likely to have been impacted by the stronger Euro. Despite the fall in the BCI, it still points to a rise in annual GDP growth from Q2’s level of 2.1%. The annual GDP growth is likely to be around 2.3% this year, the strongest since 2011.

ECB’s Mario Draghi yesterday highlighted the strength of the economy in the Eurozone but also emphasised on his expectations of inflation to remain low partly as a result of stronger Euro. He said that ECB will continue to provide as much stimulus as the economy may need. At a different speech, New York Fed President, William Dudley, stuck to the notion that low inflation in the US was impacted by temporary factors and may pick up pace in the near future. His bias appeared to be towards another rate hike in December. Futures implied probability of a December rate hike in the US now sits at 63%.

In the region, Saudi Arabia is on the road to raise money via benchmark sized bond offerings with 5yr, 10yr and 30yr tenures to fund circa $57 billion of budget deficit expected in 2017.

|

| Time | Cons |

| Time | Cons |

| US new Home sales | 18:00 | 588k | Yellen speaks on Inflation | 20:45 |

|

Source: Bloomberg

Safe haven bid on the back of increasing tension between the US and the North Korea supported sovereign bonds. Yields declined on benchmark bonds across most of the developed world with 2yr and 10yr UST yields closing lower at 1.42% (-1bp) and 2.22% (-2bps). Yields on 10yr Gilts and Bunds were also down by 2bps and 5bps to 1.333% and 0.40% respectively.

Risk aversion led to mild credit spread widening in the GCC region even though oil prices were boosted higher from news about lower supply and inventory levels. Option adjusted spread on Barclays GCC bond index rose by two bps to 138bps. 5yr CDS spreads on GCC sovereign had slight widening bias with Bahrain closing 3bps higher at 243bps and Abu Dhabi at 64bps (+2bps). That said, CDS levels on KSA remained unchanged at 90bps despite the announcement of possible new bond offering.

In the primary market, KSA has mandated banks for dollar denominated benchmark sized 5yr, 10yr and 30yr bond deals. Also Commercial Bank of Qatar is planning to issue circa $250 million in Fermosa bonds to be placed with Taiwanese investors.

JPY outperformed yesterday after finding support from safe haven bids amid political uncertainty. Over the course of the day USDJPY fell by 0.24% to 111.73, to fall for a second consecutive day and close below the 200 day moving average (112.11). Currently trading at 111.51, resistance currently stands at the 200 day moving average with support to be found at the 100 day moving average (111.09).

NZD underperforms in today’s Asia session after softer than expected economic data. A report showed that the trade balance reversed to a deficit of NZD 1234m in August, compared with a surplus of NZD 98m the previous month. As we go to print, NZDUSD trades at 0.27% lower at 0.72446. We expect a break of the 100 day MA of 0.7238 to pave the way for a more significant decline towards 0.7150.

Equity bourses around the world closed softer amid increasing geopolitical tension. Dow Jones and S&P 500 were down by quarter of a percentage and Euro Stoxx closed down by -0.10%. Asian equities are mostly trading lower this morning lead by -0.16% fall in Nikkei and -0.03% in Hang Seng.

Regional equities were mixed. General index in Dubai and Abu Dhabi were lower by more than 0.65% each, following a -1.40% decline in KSA’s Tadawul. However Qatar closed up by 0.64% and Oman was not too far behind with 0.57% increase in Muscat index. Emaar Properties and Dana Gas were amongst the most traded names in the UAE.

Brent futures surged to a new 2017 high yesterday, rallying almost 4% to close above USD 59/b. Uncertainty over the referendum in the Kurdish region of Iraq helped add some political risk momentum to prices while OPEC figures continue to sound off in positive tones about the rebalancing in the market. WTI prices also rallied strongly, closing above USD 52/b.

The rally in front month Brent has pushed the whole of the curve into a strong backwardation, with the 1-2 month spread as wide as USD 0.60/b this morning. WTI has also shifted into backwardation from March 2018 onward, albeit not as strongly as Brent. As a cautionary sign that things are not all well in the oil markets, however, the spread between WTI and Brent has widened to as much as USD 7/b and the WTI curve. Speculative positioning in Brent futures is also at elevated levels: the long to short ratio is nearly 8, its widest level since February this year.

Click here to download full publication