Recent Search

Popular Searches

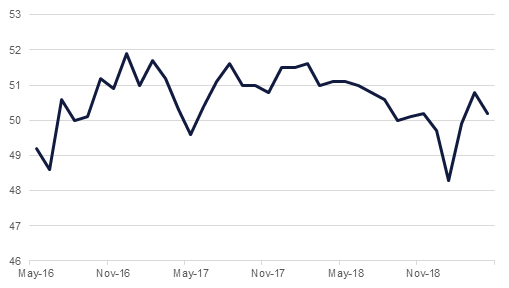

Both the official National Bureau of Statistics and the private Caixin/Markit PMI indices released this morning revealed that the Chinese recovery heralded by improved PMI readings and stronger-than-anticipated GDP growth in the first quarter has not been sustained at the same pace. The Caixin manufacturing PMI fell from 50.8 in March to 50.2 in April, missing expectations of 50.9, while the official reading declined from 50.5 to 50.1. Services also expanded at a slower rate than seen the previous month.

US personal spending grew by more than forecast in March, suggesting that consumption growth may be firmer in the second quarter than it was in the first. However, personal income growth was softer than expected last month and the core PCE deflator also came in below consensus forecasts, suggesting that inflationary pressures remain muted. The Dallas Fed Manufacturing Activity index came in well below forecasts at just 2.0 (consensus was 10.0) and the March figure was revised lower as well.

Broad money supply growth in Saudi Arabia accelerated at the fastest rate in three months in March, at 1.8% y/y. the main driver was growth in m1 (cash in circulation). Private sector credit grew 3.0% y/y last month, the same rate as in February. SAMA's net foreign assets jumped USD 493bn in March, after declining in both January and February. Year-to-date, SAMA's NFAs rose USD 3.4bn.

The IMF expects only a marginal acceleration in GCC growth this year, according to the latest regional economic outlook. Government spending is expected to provide some support but the Fund notes that the relationship between government spending and GDP growth has weakened in recent years. Fiscal break-even oil prices across the GCC have declined since 2014, reflecting fiscal consolidation efforts, except in Oman where the fiscal break-even oil price has crept up close to USD 100/b.

Source: Bloomberg,Emirates NBD Research

Source: Bloomberg,Emirates NBD Research

Treasuries drifted lower with the curve steepening slightly ahead of the Federal Reserve meeting later this week. Yields on the 2y UST, 5y UST and 10y UST closed at 2.29%, 2.31% and 2.52% respectively.

Regional bonds continue to drift higher. The YTW on the Bloomberg Barclays GCC Credit and High Yield index closed at 3.98% while credit spreads closed at 157 bps.

Lower-than expected PMI readings out of China impacted the Australian dollar as it depreciated against its primary trading partners in the major move of the morning. The AUD fall 0.2% against the USD to 0.7046. The Turkish lira, meanwhile, continues its renewed depreciation as fears over the central bank’s commitment to tighten monetary policy if necessary were renewed following its MPC meeting last week. It was trading at 5.9526 in early morning trading, lows not seen since October last year.

Developed market equities closed largely unchanged ahead of the Fed meeting later this week and amidst mixed corporate earnings. The S&P 500 index added +0.1% while the Euro Stoxx 50 index remained flat.

Regional markets closed mixed as UAE bourses closed lower while the Tadawul continued its positive run. Banking sector stocks saw profit booking with FAB losing -1.2% and Qatar First Bank dropping -2.3%. After the market closed, FAB reported Q1 2019 earnings in line with consensus estimates.

Brent futures closed broadly flat on Friday overnight, at USD 72.04/b, down just 0.2%, while WTI edged up 0.3% to USD 63.5/b as the market continued to digest the effect of US president Donald Trump’s public call on OPEC to increase production. Prices are nudging lower in early trading today as markets continue to expect higher production from Saudi Arabia and other OPEC members with capacity to increase.

Khatija Haque

Khatija Haque