Recent Search

Popular Searches

Central bank officials on both sides of the Atlantic continue to push back against the reflation narrative that has gripped markets in recent months, even in the face of significant jumps in price growth in April. Central bankers are firmly sticking to the party line that the inflationary spike will be transitory, albeit with a rising acknowledgment that ‘transitory’ is a relative term, and that for the next several months at least, inflation will likely be higher than we have seen for some time. With many data points still returning fairly mixed results the rationale for keeping policy loose remains firmly intact, and we maintain that rate hikes remain some distance off. However, as many inflationary inputs remain in effect the internal debate at MPC meetings will become more divided, with a sooner-than-signposted tapering of QE becoming a more likely prospect.

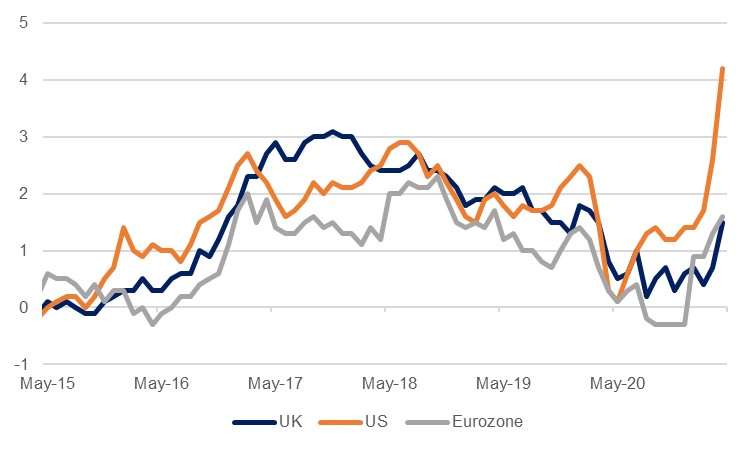

US inflation surprised significantly to the upside in April, coming in at 4.2% y/y, exceeding expectations of 3.6%. This was the fastest pace of growth since 2008, and was attributed to the slow pace of inflation in the year-ago base (as the US was first in the grips of the pandemic crisis), the reopening of the economy, and pent-up demand among consumers, many of whom have amassed considerable savings while retail and hospitality outlets have been shut, and have also benefitted from direct payment cheques associated with government pandemic support. In the UK, price growth jumped to 1.5%, itself the fastest pace since March last year, with a rise in energy prices being the standout driver. In Europe, the Eurozone inflation figure was 1.6% in April, the fastest pace in two years.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

While these latest inflation prints might not herald a return to previous extended eras of high price growth, local and global dynamics suggest that April will not be the only month where we see these elevated levels. The ongoing chip shortage which has had an inflationary effect on the automotive sector in particular is unlikely to ease any time soon given still-high demand and the risk of a lockdown in key producer Taiwan as it contends with a rise in Covid-19 cases.

Shipping will remain expensive for now, as the Shanghai containerised freight index has hit an all-time high of 2,134 in May, more than double the series average (from 2011) of 983 and up 143% from levels just prior to the pandemic. As the decade spent ironing out the overcapacity issues which followed the GFC will attest, container shipping is a notoriously unagile industry – about as swift to maneuver as the proverbial tanker – and any new tonnage ordered now (the global container shipping orderbook has risen from a series low of 8.5% of total DWT at the close of last year to a five-year high of 14.2% currently) will not launch for several years. There are similar stories playing out in energy and commodity markets, and a mismatch in jobs could see some labour market price pressures brought to bear as well.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

As these inflation figures hit markets, central bank officials repeated their assertions that this acceleration in price growth was a temporary phenomenon, driven by exceptional circumstances, and unlikely to presage a fundamental rise in inflation. Federal Reserve vice chair Richard Clarida took interviews following the US data release, and while he acknowledged surprise at the scale of the upside shock, he maintained that it was transitory. Equally, BoE Governor Andrew Bailey acknowledged that inflation would rise for several months, but also held that any acceleration would be temporary.

In any case, central bank officials are wary of repeating what are now seen as the mistakes that followed the GFC, when a hasty return to tightening policy might have been responsible for the lacklustre and protracted recovery from that crisis. The FOMC changed its policy outlook in mid-2020, now saying that it is happy to see inflation run above its long-run 2.0% target for a while as it pursues full employment, especially if inflation has undershot for a period. With the April NFP jobs report disappointing markedly to the downside, and a range of other recent data points such as retail sales growth relatively mixed, the committee remains of the view that now is not the time to be looking at tightening policy. The dot plot (which was released before the April inflation reading) shows that more committee members expect a rate hike next year than previously, but the majority view remains that any upward move will come after 2023. Similarly in the UK, the view is that while the economy is improving rapidly, there remain significant challenges.

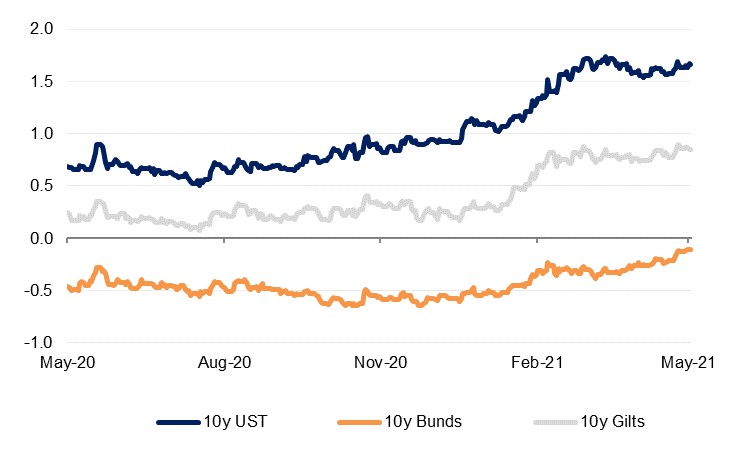

Although a rate hike remains unlikely in any of these three markets for some time, the discussion around tapering will become louder. In mid-May, Christine Lagarde reiterated earlier comments dismissing such chatter as ‘premature’, but the situation in the Eurozone has improved markedly as the bumpy start to its vaccination programme has been put behind it and the disparity between its situation and that in the US is narrowing. The rise in German 10-year bund yields to two-year high attests to this.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

At the BoE’s May meeting, outgoing Chief Economist Andy Haldane was a lone vote against maintaining asset purchases to the target of GBP 895bn, arguing that it should be slimmed down by GBP 50bn owing to inflation concerns, but this view could become more prevalent as inflation data comes in. The bank did decide to slow the pace of its purchases but stated that this was a purely operational move. Meanwhile, the latest FOMC minutes, from the April meeting, showed an increasing willingness amongst committee members to discuss tapering of QE at upcoming meetings. Whenever these moves are taken they will likely be well signposted, with policymakers cautious to avoid a repetition of the moves in yields seen during the 2013 taper tantrum.

Daniel Richards

Daniel Richards