Recent Search

Popular Searches

Theresa May is scheduled to meet with German Chancellor Merkel and French President Macron today, after speaking to other EU leaders last night. "Technical talks" between the government and the Labour Party also continued last night, in a bid to reach a deal both sides could support. A "core" group of EU leaders (including Merkel and Macron) is scheduled to meet ahead of the main summit on Wednesday, where the bloc is expected to agree to a further extension for the UK in order to avoid a no-deal exit at the end of this week. The length of the extension remains unclear, with the EU signalling its preference for a longer delay, while the British government has requested a delay only to the end of June.

Saudi Aramco's first ever bond issue is likely to be priced today, with the oil company expected to raise at least USD 10bn in six tranches ranging from three to thirty years. Given the strong initial demand from investors - Bloomberg reports that at least USD 40bn in orders have been received - the pricing of Aramco's bonds may be tighter than the sovereign. The money raised will likely go towards financing Aramco's acquisition of SABIC shares from the Public Investment Fund (PIF).

The Aramco/ SABIC transaction is expected to yield USD 70bn for PIF to invest both domestically and abroad, to support the diversification of the Saudi economy and reduce the Kingdom's reliance on oil exports as the main source of budget revenue.

Investor sentiment in the Eurozone has improved in April, hitting its highest level since November. The Sentix survey of investor sentiment rose to -0.3 in April from -2.2 a month earlier while the expectations component improved a third month running. Conditions in the major Eurozone economies remain lackluster: German trade data for February showed a decline in both exports and imports of 1.3% m/m and 1.6% m/m respectively, both weaker than market expectations. The improvement in investor sentiment may therefore reflect a general easing of trade tensions between the US and China more than regional factors in Europe.

Source: IEA, EIKON, Emirates NBD Research

Source: IEA, EIKON, Emirates NBD Research

Treasuries ended the day lower amid focus on Saudi Aramco’s jumbo offering and ahead of inflation data later in the week. Yields on the 2y UST, 5y UST and 10y UST closed at 2.36% (+2 bps), 2.33% (+1 bps) and 2.52% (+2 bps) respectively.

Saudi Aramco is looking to raise USD 10bn in an offering across tranches of 3y, 5y, 10y, 20y and 30y. At the time of writing, the company had received orders of at least USD 40bn for its offering.

Elsewhere, Carlyle has agreed to buy a 30% stake in Cepsa from Mubadala for USD 3.6bn.

This morning the dollar is trading slightly softer, the Dolllar Index (DXY) having fallen 0.05% to 96.602. This loss adds to earier losses realized on Monday following a contraction in U.S. factory orders.

With no first tier economic data expected today, we expect currency markets to be driven by risk appetite.

Developed market equities closed mixed as investors’ locked in recent gains. The S&P 500 index (+0.1%) drifted while the Euro Stoxx 600 index dropped -0.2%.

Regional equities continued to build on their recent gains. The DFM index and the Tadawul added +0.6% and +0.3% respectively. Dubai Islamic Bank added +1.6% amid unconfirmed reports that the bank is looking to acquire Noor Islamic Bank. Elsewhere, Almarai gained +4.8% despite reporting mixed set of Q1 2019 earnings.

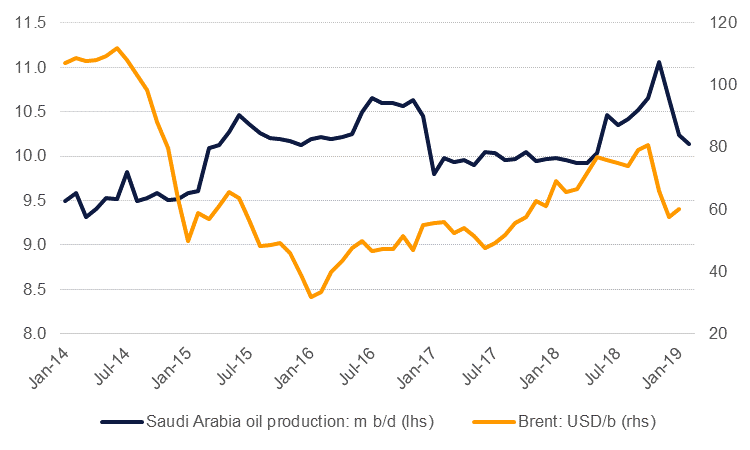

Oil markets continued to push higher at the start of the week with WTI gaining more than 2% to close at USD 64.40/b while Brent added 1% to end the day above USD 71/b. There was mixed commentary from oil market officials overnight, tempering the prospect of the OPEC+ production cut agreement lasting until the end of the year. Saudi Arabia’s energy minister Khalid al Falih said yesterday that oil markets were on their way to balancing, helped by OPEC’s strong adherence to production cuts that took effect at the start of 2019.

Al Falih said that he didn’t think there was a case for Saudi Arabia continuing to to cut as deep as it has been doing as it has been over-delivering on its share of production cuts. Al Falih indicated it was too early to say if OPEC+ would end its production cut agreement but would use a meeting in May to assess market conditions on whether to deepen, extend or end cuts.

Meanwhile the head of Russia’s sovereign wealth fund indicated that the cuts could come to end by June as markets were already rebalncing. The risk of a deeper deficit in coming months will become more apparent should the Trump administration choose not to extend waivers on Iran sanctions in May.

Khatija Haque

Khatija Haque